The Steel and Engineering Industries Federation of Southern Africa (SEIFSA) is the principal advocate for companies operating in the metals and engineering sector. SEIFSA as a federation represents 18 employer associations, who collectively represent in excess of 1100 companies. These companies employ 170 000 employees in the sector.

METALS AND ENGINEERING SECTOR FACT AND FIGURES

The metals and engineering sector constitutes 25.6% of the total manufacturing sector. The sector is an integral part of the global and domestic economy and a crucial supplier of inputs into sectors such as mining, the automotive sector, construction and other manufacturing industries.

| Sub-Sector | % of Manfacturing |

| Plastic products | 2,29 |

| Basic iron and steel products | 2,82 |

| Non-ferrous metal products | 3,26 |

| Structural metal products | 1,98 |

| Other fabricated metal products | 3,35 |

| General purpose machinery | 3,46 |

| Special purpose machinery | 3,87 |

| Household Appliances | 0,73 |

| Electrical machinery and apparatus | 2,31 |

| Bodies for motor vehicles, trailers and semi-trailers | 0,71 |

| Other transport equipment | 1,37 |

| Total M & E Sector | 26,15 |

Source: Statistics South Africa

The important facts and figures relating to the metals and engineering sector are contained below:

| Dashboard: Comparison of the 2020 to 2021, in the M&E Sector | ||

| ECONOMIC VARIABLE | 2020 | 2021 |

| M&E production (% growth) | -12,8% | 10,7% |

| M&E production sales (Rand value) | R633,6 billion | R804,1 billion |

| M&E capacity utilization (%) | 67,1% | 76,2% |

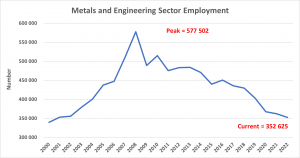

| M&E Employment (number) | 361 983 | 352 625 |

| Total M&E employment share (%) | 35,8% | 35,9% |

| M&E Export value (Rand billion) | R371, 3 billion | R458,8 billion |

| M&E Import value (Rand billion) | R432 billion | R531,5 billion |

| M&E Net trade balance (Rand value) | -R60,7 billion | -R72,7 billion |

| M&E Gross earnings (Rand current prices) | R104,5 billion | **R108,2 billion |

Source: Statistics South Africa, SARS, MIBFA

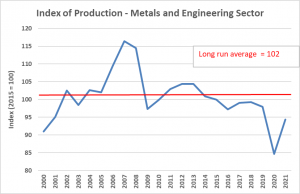

The graphs below are the most effective way of communicating the distress experienced in the sector. Production trends have been on a persistent downward trajectory since the 2008/9 global financial crisis from which the sector has never recovered. Naturally, the sector was not spared from the economic disruption of covid-19.

THE IMPORTANT ROLE OF THE STATE

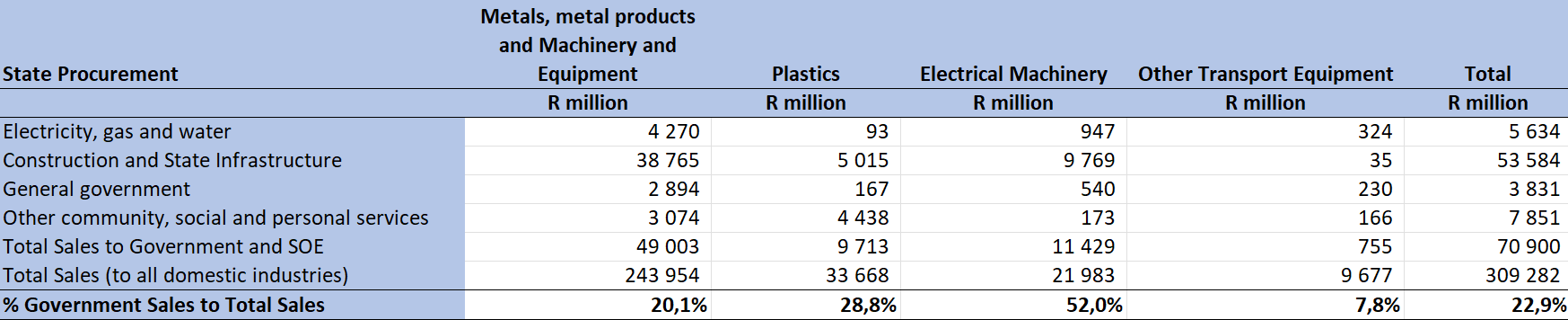

State organs namely general government, state owned entities and the country’s 278 municipalities are key markets to which the metals and engineering sector supplies products. In 2020, state organs procurement amounted to R70.9 billion, or 22.9% of total domestic sales from the sector. Notably, state procurement from the electrical machinery sub-sector accounts for more than half (52%) of domestic sales. The importance of state procurement from the metals and engineering sector has necessitated that SEIFSA prepare this submission in response to the draft Preferential Procurement Regulations (2022) issued by the National Treasury for public comment. Public procurement has the potential to stimulate domestic demand for products from the metals and engineering sector, which will support economic and industrial development. State procurement is an important domestic demand anchor for the sector and contributes to facilitating greater economies of scale, which in turn contributes to competitiveness and export opportunities.

The conventional GDP equation (GDP = Consumption + Private-Investment + Government-Investment + (Exports – Imports) proposes that large scale private investment, which is inversely related to taxes and interest rates, drives economic growth. However, in reality private sector investment is also driven by “herd” instincts, which are naturally volatile and in turn makes the overall GDP outcome volatile. Greater domestic investment (and domestic procurement) by the state introduces a stable anchor on which the rest of the GDP components can be built on, thereby creating a stable and sustainable GDP trajectory, (Mariana Mazzucato – Entrepreneurial State, 2013).

Given the above context as a departure point and the importance of state procurement for the metals and engineering sector, SEIFSA submits that the draft preferential procurement regulations published by National Treasury run counter to the industrialisation aspirations of the country, have the potential to reverse the historic efforts that have been invested into processes of developing industry master plans and designation efforts. The regulations will also create an untenable environment wherein local companies will have to contend with multiple un-standardised procurement policies from different state organs.

The material aspects of SEIFSA’s submission to the draft Preferential Procurement Regulations (2022) are listed below:

- It is important to stress that SEIFSA’s concerns are not with the decision of the Supreme Court of Appeal (SCA) or the Constitutional Court on the Preferential Procurement Regulations. It is important that all regulations that direct the functioning of state organs are consistent with the country’s constitution. However, the concerns listed below relate to National Treasury’s interpretation of the court decision as inferred by the published draft Preferential Procurement Regulations 2022.

- The omission of local content, local production or designated products in the draft regulations, to give some preference to local companies from public procurement is a missed opportunity to leverage state procurement as an instrument to drive domestic industrialisation.

- To remove any forms of preference for domestic companies, in the absence of initially dealing with aspects that relate to the cost of doing business in the country is akin to putting the proverbial cart before the horse. The unfortunate outcome that is likely to manifest is that domestic companies will be unable to compete with imported products leading to further de-industrialisation. This is not to advocate that local procurement by the state and industrialisation should pursued at all costs and at the cost of competitiveness, however, the domestic input cost structures creates an unfavourable environment for companies to compete with imported products. The focus should be to create a suite of incentives from tax rates to industrial incentives that will assist domestic companies to compete if the preference for local procurement from domestic companies were to be removed.

- Efforts to revive the unprecedented levels of decline in the economic performance of the metals and engineering sector are contained in the Steel Master Plan (SMP), which is an industry initiative by government, labour and the private sector. The SMP envisages leveraging the country’s infrastructure drive and localisation by state owned entities as instruments to boost demand for locally produced products. The plan also proposes designation of locally produced products for public procurement as a stability measure that can be implemented in the short-term to support demand for local products. The draft preferential procurement regulations in the current form would in essence reverse all the efforts that have been invested by the sector in the development of the SMP. This point is possibly applicable to all the other sector master plans. This raises the very worrying prospect of inconsistent policy formulation in the state, where different national departments develop and pursue fundamentally different policy directions.

- In the absence of explicit regulations guiding state organs on the procurement policy, the Preferential Procurement Policy Framework Act (PPPFA) state that state organs will develop their own procurement policies based on socio-economic considerations listed in the Reconstruction and Development Programme (RDP) of 1994. This means that organs of state will develop their own measures for industrial, economic development and socio-economic aspirations. While these measures will support local economic development, SEIFSA submits that devolving this obligation to each state organ to create its own procurement policy will create an untenable administrative and compliance environment for domestic companies. It is paramount that National Treasury develops a national guideline for state organs to comply with in the development of their procurement policies. This will be important for institutional coordination and alignment across the multiple state organs. It will also make monitoring and enforcement of regulations possible. Coherence and uniformity should be the basis on which national regulations are developed.

- SEIFSA recommends that given the importance of these regulations and the possible unintended consequences that would manifest if they are to be passed in their current form, National Treasury should embark on an extensive consultation process in the development of these regulations. While it is acknowledged that regulations are an executive function that govern day-to-day functioning of the state, we submit that the policy implications of these regulations extend far beyond the aspects that they seek to regulate. As a result, SEIFSA recommends a thorough consultation process for these regulations be implemented through the NEDLAC processes. This will allow National Treasury the opportunity to receive much more detailed inputs from the social partners represented on the NEDLAC structures.

Thank you for the opportunity to make representation on behalf of the metals and engineering sector. We trust that our inputs will receive your favourable consideration.