SEIFSA report outlines risks for Metals & Engineering sector in 2024

The outlook for the South African Metals & Engineering sector in 2024 is not as bleak as it was last year, but risks — both local and global — remain high, according to the State of the Metals and Engineering Sector Report 2024, which the Steel and Engineering Industries Federation of Southern Africa (SEIFSA) released this week.

The report, which was presented in a webinar on February 20, examines the current state of the Metals & Engineering (M&E) sector amid moderating inflation and heightened geopolitical tension.

SEIFSA chief operating officer Tafadzwa Chibanguza, says “the geopolitical temperature is high, with wars in Europe and the Middle East and the subsequent attacks in the Red Sea.”

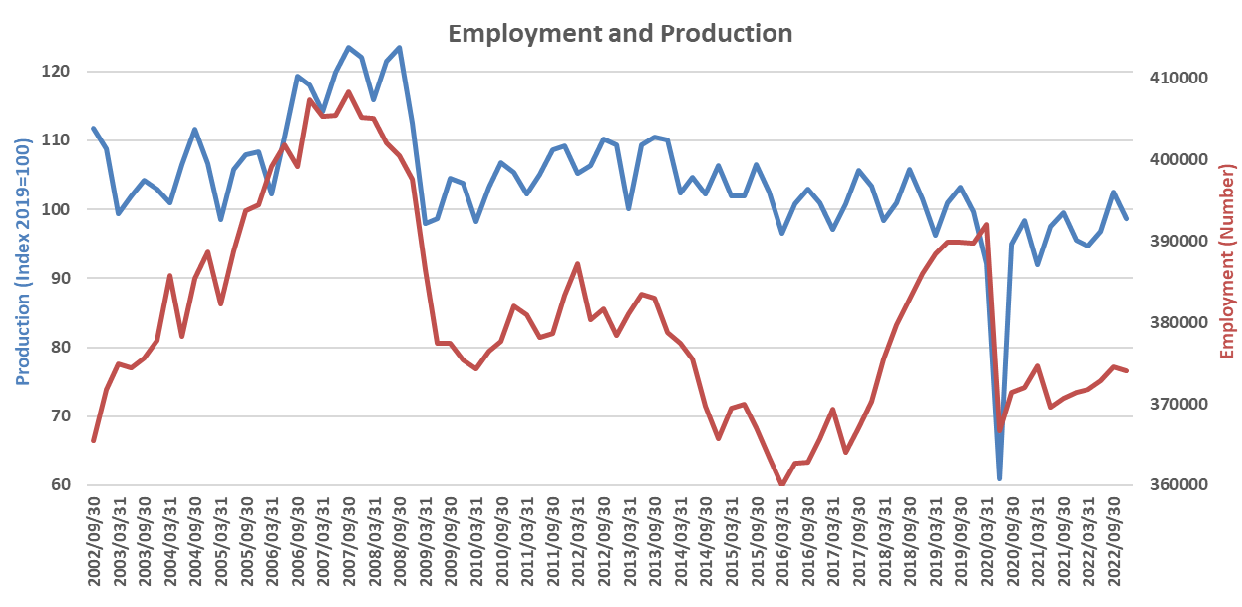

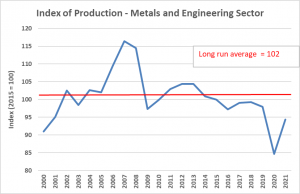

Aggregate production increased by 1.7% in 2023, slightly higher than the 1.5% in 2022 but still remains 18% below where it was in 2008/2009.

“Production has also not sustainably attained its pre-Covid lockdown levels and has been oscillating between 1-2 index points around this level,” Chibanguza said.

This is amid the “expectation for global economic growth to flatline into the medium term, which presents a neutral perspective on demand prospects from the external environment. Growth is primary tilted in favour of the advanced economies, which presents limited export opportunities given that Sub-Saharan Africa is the largest export market for the sector,” says Chibanguza.

Geopolitical risks include the ongoing wars in Europe and the Middle East, while locally the sector faces persistent load-shedding, logistical challenges, including the crisis at Transnet, deteriorating service delivery at municipal level, looming wage negotiations and the uncertainty of an election year along with the political noise that leads up to the event, he says.

“Whatever the outcome of the election, it presents risk as a lot of work has been done in terms of macro-economic policy around for example energy and public procurement. . A new administration means dealing with new members of parliament and a new cabinet.”

On the positive side, inflation is subsiding faster than expected, particularly in the advanced economies, which should allow for hard currency rate cuts, which in turn should set the scene for global monetary policy, says Chibanguza.

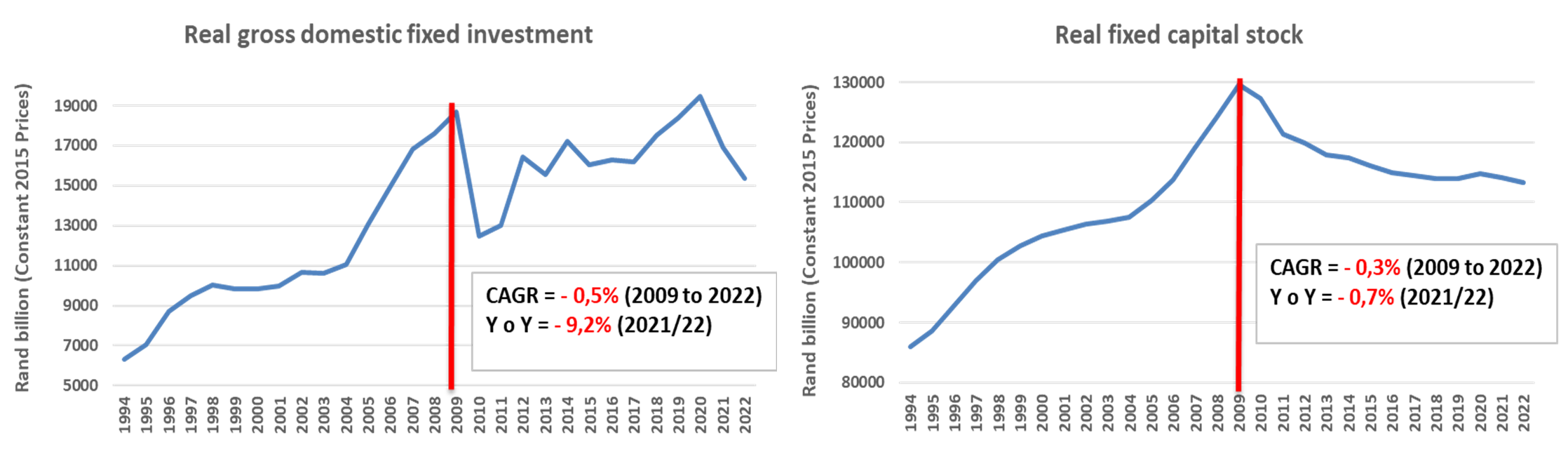

Global inflation is set to decline from 6.8% in 2023 to 5.8% in 2024, and 4.4% in 2025, which should set the scene for interest rates to start coming down. Declining interest rates presents a scenario for investment in the economy to hopefully start picking up which in turn is a good demand source for the metals and engineering sector. It will also decrease the pressure on debt service costs for the state, possibly creating fiscal headroom, for state spend into the economy, which again is another important source of demand for the sector. Lastly, lower interest rates should also provide room for companies in the metals and engineering sector to increase investments into their operations, which is particularly important given the negative net investment trend that has underpinned the sector since 2008, which has also resulted in the sectors fixed capital stock deteriorating at a rate of 0.8% (CAGR) over the same period.

While work has been done to revive the economy, reforms take time for their full effect to be realised, but unfortunately the sectors potential will remain constrained for as long as too many local companies remain in survival mode due to the array of challenges they face.

Steel and Engineering Sector on the Precipice of an Unprecedented Jobs Crisis

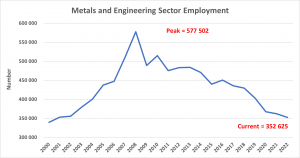

The employment trends in the metals and engineering sector are an important indicator for the underlying structural constraints that have plagued the sector for the last decade and a half. The sector currently employs 362 871 people, which is a significant drop from the 577 507 people employed in 2008. This equates to a decline of 214 636 jobs, or 37.2% and when measured on a compound basis, represents a 2.9% decline per annum over this period.

Employment in the sector has decreased at double the rate production has decreased over the same period. Considering the steel sectors induced economic multiplier of 2.7 times, the employment multiplier of 6 times and the dependency ratio of between 7 to 10 people relying on each formal job, the sectors employment trends spell wide scale social and economic disaster.

The steel and engineering sector is crucial to the South African economy, it is the backbone of the country’s industrial base which is akin to none on the continent. Apart from the traditional arguments of the virtues of the manufacturing sector which include the productivity gains to economic growth, higher income elasticity of demand for manufactured goods and the spill over of growth to non-manufacturing sectors in response to growth in manufacturing output, the steel and engineering sector is also a strategic avenue through which the country converts its vast mineral endowment to final engineered products. This locks in a higher degree of value add domestically.

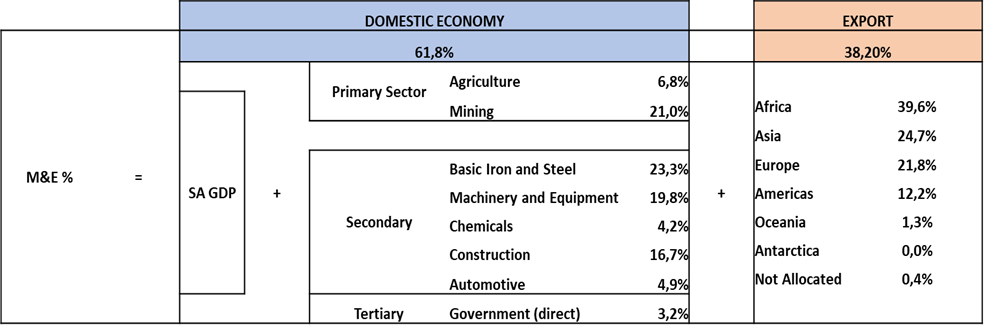

The value chain represented in the sector constitutes the entire metals value chain from metal production (ferrous and non-ferrous), merchants and service centres, metal fabrication to heavy and light engineering. The sector is a crucial supplier of inputs into sectors such as agriculture, mining, the automotive sector, construction, the electricity supply industry across all its facets, logistics and water sectors. Moreover, the sector is export intensive, with 40% of total production being exported, raising the country’s foreign exchange receipts by USD $20 billion annually.

Despite the sectors far-reaching impact and diversified demand profile the innate potential is unfortunately not being realised. The recent announcement by ArcelorMittal South Africa (AMSA) on the closure of its operations in Newcastle and Vereeniging, as well as ArcelorMittal Rail and Structural bears testament to this. The prospect of this development materialising is a major cause of concern which will only add to exacerbating the downward spiral to employment in the sector.

The long products operations under consideration include the country’s only local mill capable of producing long steel from iron ore which are critical in industries such as construction, automotive, mining, electro-technical, electricity transmission, rail, wire and fasteners industry. The reliance of these downstream industries is not a preference question but rather higher quality and safety specifications. Faced with the prospect of a lack of domestic supply, these downstream industries will have no alternative but to look to import their feedstock, which translates to the loss of much needed domestic jobs, further deepening the unemployment crisis.

The intrinsic nature of risk mitigation for businesses is to act on eliminating potential risks before they become events, meaning that the horse may have already bolted in a number of instances. When import alternatives are bedded down, they are likely to become entrenched thereby structurally altering the industrial landscape permanently, to the detriment of South Africa’s industrialisation aspirations and fortunes.

Of the 362 871 employed in the sector, the downstream industries account for 90% of the employment with the balance being employed in the upstream. This number has evolved from 80% (downstream) and 20% (upstream) over the last 15 years. The sector employed 577 507 people at the peak of 2008. Although the job losses have been felt across the entire value chain, they have mostly been concentrated in the downstream industries, which have accounted for 60.2% of the losses recorded over this period. The point being that the propensity of the sectors employment losses, as a result of the structural vulnerabilities and headwinds faced by the sector, mostly materialise through employment losses in the downstream industries. It is therefore reasonable to conclude that the impact of the plant closures will mostly be felt in the downstream where the bulk of employment resides. Of even greater concern is that a number of companies in the downstream have started estimating the business cases of importing their final product as opposed to semi-finished products (billets, blooms, etc.,) for further processing locally. This will have even wider employment ramifications by eliminating other intermediate processes like forging, galvanising and packaging, thereby converting many existing factories into distribution warehouses.

Another important structural dynamic emanating from the employment trends is a continued decoupling of the relationship between employment and production i.e., increases in production is becoming a less sufficient condition for employment creation. The latest estimates indicate that a 4.7% increase in production is required to induce a 1% increase in employment. An alternative approach to confirm the analysis is the fact that between 2008 and 2023 production has decreased at a rate of -1.3% (CAGR) while employment has decreased at -2.9% (CAGR). Given globalisation and greater levels of mechanisation, this phenomenon is not entirely surprising, however, the data indicates that periods of deep structural adjustment, like the 2007/8 global financial crisis, COVID lockdowns and periods of production disruption as a result of industrial action have tended to worsen the trend. The AMSA plant closures, which will present a major headwind for the sector, followed by a deep and painful structural adjustment, will deepen the decoupling pattern.

In the final analysis, the reasons for the AMSA plant closure are structural, namely: low economic growth, anaemic gross fixed capital formation, electricity and logistics challenges. These are factors faced by companies in the entire value chain and without urgent intervention and reform are unlikely to be resolved in the medium term. It is conceivable therefore that in the absence of reform, the rate of employment declines observed thus far can be projected into the medium term with some modifying factors applied to account for the AMSA closure.

Taking into account the 3500 employees that will be directly affected by the plant closures, projecting the 2.9% (CAGR) rate of decline across the entire steel and engineering sectors employment and applying the steel sector employment multiplier, on a five-year horizon, SEIFSA’s estimates the employment losses could amount to a staggering 293 754 direct and indirect job losses.

This is an outcome that South Africa, given its already untenable unemployment rate, can ill-afford. Doing everything possible to finding lasting solutions to averting the announced plant closures should dominate our and governments agenda, failing which industry and the economy will be left to deal with a catastrophic socioeconomic jobs crisis of unimaginable proportions.

SEIFSA load shedding impact assessment on the Metals and Engineering Sector

The energy crisis that is gripping South Africa presents the most significant risk and binding constraint to the economic prospects of the country. The crisis not only has implications on the immediate survival of companies but also on the long-term implications regarding the investment prospects of the country. The crisis has been particularly damaging on the metals and engineering sector, a sector which is the backbone of industrialisation and to which electricity, particularly baseload electricity, is fundamental to its survival.

SEIFSA represents 18 Employer Associations, who collectively represent in excess of 1 300 companies and employ in excess of 170 000 employees in the metals and engineering (M&E) sector. The M&E sector constitutes 26.5% of the manufacturing sector, based on output, and 2.6% the country’s gross domestic product (GDP) on a value-add basis. As at December 2022 the sector employed 374 496 (of which 217 618 are factory workers) who are employed in approximately 10 00 companies.

It is important to highlight, in brief, the historic context in which this survey is conducted. The M&E sector has been in a structural recession since the global financial crisis of 2008/9, with production recording a 1.2% contraction on a compound annual basis over this 15-year period. Given the less supportive global economic environment and the impact of domestic rigidities, chiefly the energy crisis, production in the sector is expected to contract further by 2.2% in 2023. Unfortunately, employment in the sector has also mirrored the production trends contracting at -1.1% (CAGR) and contributing to the country’s unemployment crisis. These trends are contained in the graph below. The Covid-19 induced lockdowns presented a major economic shock to the sector and although the production levels recovered (still 1% below pre-covid levels), employment trends have not (4.6% below pre-covid levels). Increasingly the sector has observed a weakening relationship between production and employment, meaning improving production outcomes are no longer a necessary condition for employment creation.

Source: SEIFSA, Statistics South Africa

The intensifying electricity crisis now presents the most prevalent economic risk to the sector:

It is in this context that SEIFSA undertook to survey its affiliated membership and developed this load-shedding impact assessment. This survey measures the impact of the energy crisis over a 12-month period (February 2022 to February 2023) across four main parameters, namely:

1. Employment;

2. Production;

3. Investment;

4. An analysis of the alternative energy investments made by the sector; and

5. Impact to Input costs.

The survey garnered a positive response, with 206 companies responding. The survey parameters are included below:

| Category | Survey Sample |

| Number of respondents (companies) | 206 |

| Total Employee Count (from responding companies) | 37 284 |

| Average number of employees (proxy for company size) | 184 |

| % of sample to total SEIFSA member employee headcount | 26.5% |

| % of sample to total M&E Sector employee headcount | 9.9% |

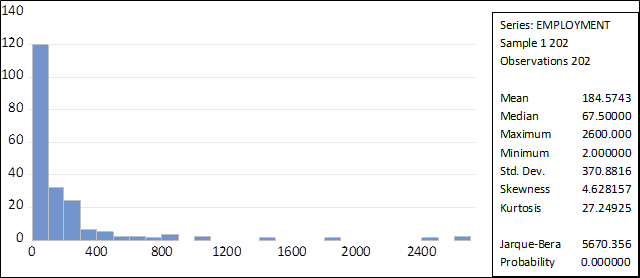

The employee headcount is the pivot variable for the purposes of consolidating the statistics, particularly the weighted outcomes. The companies that responded to the survey vary in head count from 2 employees to 2600 employees.

The straight average headcount across the sample is 184 employees yielding a good mix between large, medium and small companies. The definition of small to medium companies in the sector, based on headcount, is 50 employees or less. These companies represent 41.3% of the sample. The histogram below indicates the distribution of the company sizes relative to employment:

The consolidated results of the survey are contained in the table on the next page.

It is necessary to bear in mind that these results are from a sample representing 10% of the sector (measured on an employment metric).

Theoretically, the outcomes, particularly the absolute numbers, could be multiplied by 10 to get the full impact on the sector.

Consolidated results of the survey:

Employment:

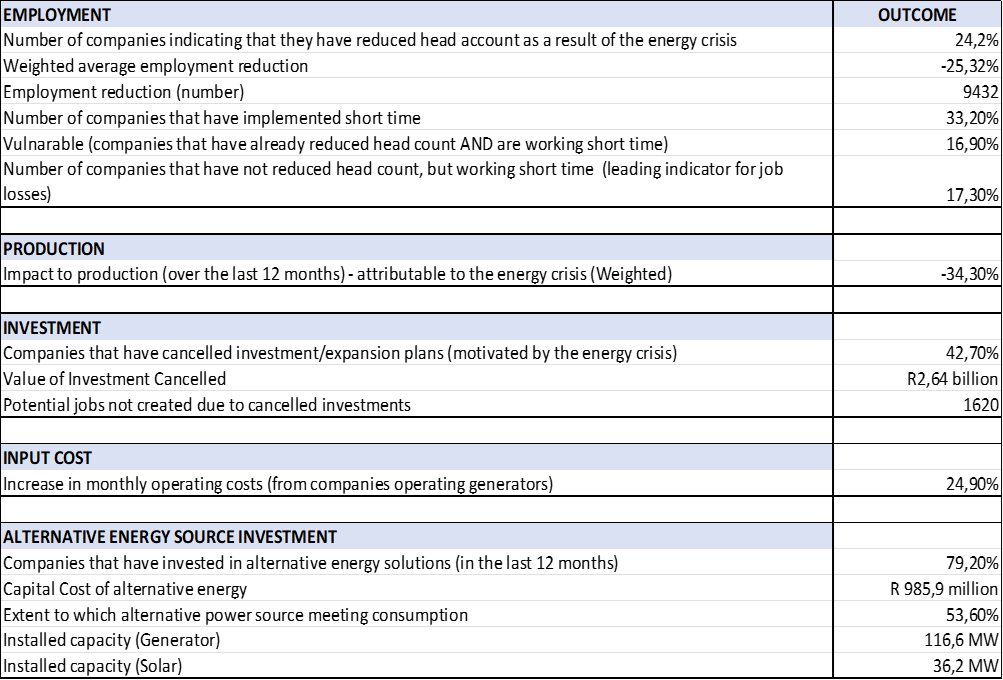

• The employment losses, mostly attributable to companies responding to the energy crisis over the reference period, indicate some very concerning trends.

• A quarter of companies indicated that they have had to reduce head count in response to the electricity crisis, by as much as a quarter of their employment, equating to 9 432 people.

• A third of the sample indicated that they are working short-time due to the electricity crisis.

• An even more concerning outcome is the fact that half (16.9%) of those companies that are implementing short time have already reduced head count.

• We assign the status of “vulnerable” to these companies, while the other half (17.3%) have not reduced head count, however, short time is a good leading indicator to track for potential future job losses.

Production:

• The respondents to the survey indicated production declines as much as 34.2% (weighted) as a result of the electricity crisis.

• Based on the model in the table below, SEIFSA has calculated that production in the sector is estimated to contract by 2.2% in 2023.

• However, factoring in the results from this survey, the forecast for the 2023 year deteriorates to – 5.3% for the 2023 year.

Investment:

• The long-term implications of this energy crisis to the future prospects of the sector are devastating.

• Over the last 15 years, net-investment into the sector has been on the decline, which has led to the value of fixed capital stock deteriorating at -0.3% (CAGR), threatening the competitiveness of the sector.

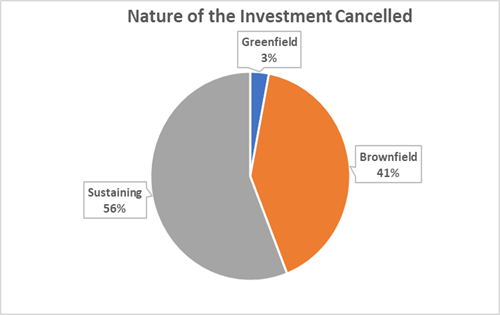

• It is therefore concerning that 42.6% of companies have indicated that they have cancelled investment and/or expansion plans owing to the uncertainty presented by the electricity crisis.

• The value of these investments amounts to R2.64 billion with the potential of creating 1 620 new jobs. The split of the nature of investment is included below.

An analysis of the alternative energy investments made by the sector:

• 79.2% of companies indicated that they have had to install alternative electricity sources in the last 12 months to counter the pressing challenge presented by the electricity crisis.

• The combined value of this investment is R985 million. This number if considerable when considering that it accounts for 37% of the value of investments cancelled. This again highlights the point that SEIFSA has repeatedly stressed that companies are sacrificing scarce long-term capital to fulfil an immediate survival, presenting long-term adverse implications regarding the sustainability of the sector.

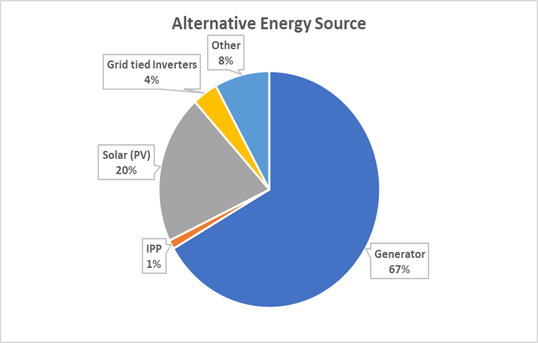

• The breakdown of the alternative technology source invested into is contained in the pie chart below. It is not surprising that given the relatively intense electricity consumption nature of the sector, the most practical alternative energy sources are generators representing 67%.

• Solar accounts for 20% of the investment made. It should however be borne in mind that this survey was done prior to the announcement of the 125% tax incentive afforded to companies in the February 2023 National Budget. This incentive should result in an increase in the up-take of solar an alternative source, however, the electricity consumption profile of the sector remains a limitation to solar being a full-scale option.

• On aggregate the companies have a generator installed capacity of 116MW, while that of solar is 36.2%.

• The respondents have registered very limited ability to feed-in any excess electricity generated from their solar installations, largely because of the fact that the solar installations have been put in as a marginal hedge or top-up to their baseload needs. This picture may well change given the 125% tax incentive, although to a limited degree, because the sectors electricity consumption pattern is the main determinant for the technology deployed.

Input Costs:

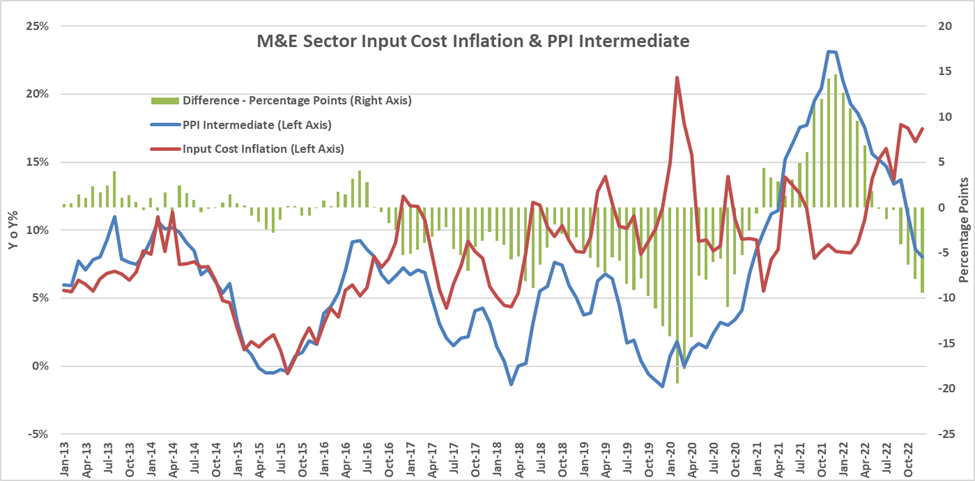

• On a weighted average basis, companies have indicated increases to monthly operating costs to the extent of 24.9% from the extensive use of generators.

• This does not bode well for a sector whose input costs are running at 17.6% (y o y - February 2023).

• Factoring in the results of the survey to the input cost model results in input costs increasing by 1.7 percentage points to 19.3% for the sector.

• The less supportive demand environment means that these companies cannot easily pass on these costs, thereby resulting in considerable margin squeeze and ultimately long-term sustainability.

We would like to thank the SEIFSA affiliated membership who have taken the time to complete this load shedding impact assessment survey.

The results of the survey are extremely valuable in providing tangible and quantifiable results which are necessary in various engagements SEIFSA will be having with key stakeholders responsible for resolving South Africa’s gripping electricity crisis.

Preferential Procurement Regulations and the Public Procurement Bill

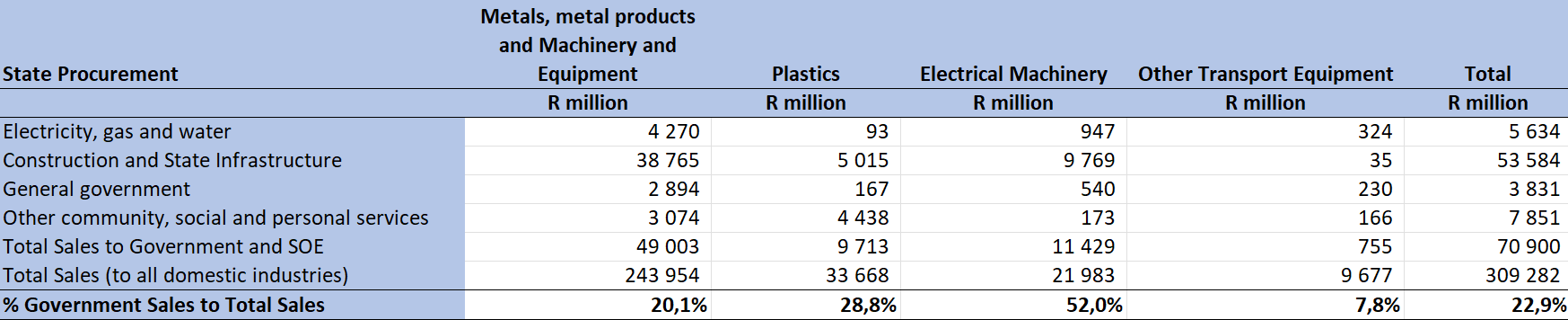

Public procurement or sales to the government from the metals and engineering sector constitutes 22.9% of total domestic sales. However, for some sub-sectors, like electrical machinery, sales to state organs is as much as 55% of domestic sales.

Given the importance of public procurement for the sector, SEIFSA has been actively involved in making national representations on behalf of the metals and engineering sector to the Public Procurement Bill and the Preferential Procurement Regulations.

Regarding the former, SEIFSA was part of the Business Unity South Africa (BUSA) business delegation that consulted on the bill at NEDLAC for the last six months. On the draft Preferential Procurement Regulations that were published for public comment on the 10th of March 2022, SEIFSA prepared a substantial written submission commenting on these regulations. Subsequently, National Treasury published the Preferential Procurement Regulations on the 4th of November 2022, with an effective date of 16 January 2023.

We have studied the published Preferential Procurement Regulations with grave concerns, particularly over the fact that National Treasury has opted to maintain the position that was contained in the draft regulations that each state organ will be given the responsibility to develop and decide their own procurement policies, particularly as it relates to the socio-economic considerations.

The SEIFSA submission warned that devolving this obligation to each state organ will create an untenable administrative and compliance environment for domestic companies. The administrative and compliance costs for a company supplying the same product to two or more state organs, who may pursue very different socio-economic agendas, will be exorbitant and punitive.

The submission suggested that National Treasury should develop a national guideline for state organs to comply with in the development of their procurement policies. This is important for institutional coordination and alignment across the multiple state organs. It will also make monitoring and enforcement of regulations possible. Coherence and uniformity should be the basis on which national regulations are developed.

The other concern is the fact that National Treasury have indicated that these Preferential Procurement regulations are a stop-gap policy instrument that will be in place until the Public Procurement Bill is promulgated. The Preferential Procurement Regulations will be in effect from 16 January 2023 and National Treasury anticipates the Public Procurement Bill to be presented before Parliament by the end of calendar year 2022 or before the end of this fiscal year (February 2023).

The concern here is that based on historic experience with bills going through the Parliament, National Council of Provinces (NCOP), promulgation and signature by the President (who may also send the bill back through the Parliamentary process for one or other issue) generally takes a long time. One can anticipate that the importance of this bill particularly given the approximately R800 billion to R1 trillion per annum of state spend that it will govern over and all the possible socio-economic considerations that are associated, the parliamentary process will not be a roughshod process. All the while the costly, uncertain and disruptive environment that the Preferential Procurement Regulations potentially create will be the prevailing reality for suppliers to the state.

The unintended consequence of this approach that has been adopted by National Treasury will likely be one where companies may well adopt a wait-and-see approach, which will itself have adverse consequences from the point of view of investment decisions that may be delayed. This again is an example of the own-goals that the country has become accustomed to scoring.

Tafadzwa Chibanguza

Chief Operating Officer

SEIFSA sees significant headwinds for the steel sector

It’s been a challenging time for the metals and engineering industries recovering from the effects of the COVID-19 pandemic, unprecedented inflation, rising fuel prices, devasting floods and persistent loadshedding. All businesses have been impacted by these events. The global economic outlook has deteriorated significantly since Russia invaded Ukraine. Growth forecasts have been revised lower with each iteration while inflation has been revised upwards.

During Q1 2022, inflationary pressures were already building in the global economy, however, this was initially driven by aggregate demand increasing faster than supply chains could respond. The invasion of Ukraine by Russia in February 2022 set the proverbial cat amongst the pigeons in economic and inflation terms.

In the spectrum of leading, coinciding and lagging economic indicators, the metals and engineering sector is classified as coinciding. That is, its performance is indicative of the prevailing economic fundamentals. It is also extremely sensitive to these prevailing global and domestic economic events. To this end, our estimates already point to production in the sector contracting by between -1.1% to -1.3% in Q2 2022, with notable downside risks for the full year’s outlook.

This view is informed by a number themes that are shaping the global and domestic economic fundamentals. These include the aggressive monetary policy tightening in the US, in response to multi-year record inflation outcomes recorded in that country. The on-going Russia-Ukraine war and its implications for the European Union. A concerning development is the weaponizing of gas supply by Russia to Germany, which will have recessionary consequences for Germany, the largest economy in the EU and South Africa’s second largest trading partner. The dominance of Russia and Ukraine in the food inputs and commodity complex is driving inflationary pressure globally, reinforcing the need for central banks around the world to increase interest rates. China’s aggressive zero-covid policy, in which the last round of lockdowns has affected the economic hubs of Shanghai and Beijing have contributed to a slowing global economy.

These themes will continue to dominate the global economic narrative and the slowing of global economic growth. Steel production is highly correlated with economic growth and the early warnings signs of a slowing growth rate are evident in the reduction of iron ore prices, a key ingredient in steel production.

In dollar terms iron ore price have decreased 28.6% year to date 2022 and down 49.3% year-on-year to July 2022. This is despite a reduction in sea-borne supply from Ukraine. Domestically basic iron and steel sales declined by 8.1% year to date, other fabricated metals declined 8.5% and structural steel products declined 1% over the same period.

Compounding the global headwinds are weak domestic fundamentals that are also feeding into the outlook. The energy crisis, which was the worst on record in Q2 2022, is a major constraint and risk to the outlook. Electricity availability is an essential input into the metals and engineering sector. The sector is comprised of energy intensive users of electricity who have to cut production due to electricity curtailment. Whilst the sector also comprises producers that are less energy intensive, load-shedding causes a complete halt to operations.

The state of local government and the lack of service delivery is another major constraint. Companies in the metals and engineering sector are spread across the length and breadth of the country and are adversely affected by service delivery failure at local government level. The inefficiencies of local government breed costs for producers eroding their competitiveness. It goes without saying that, now, more than ever before a national strategy on industrialisation is needed to stabilise and reignite the metals and engineering sector, which must include an aggressive infrastructure programme and a dedicated focus on economic reform rolled-out in partnership with the private sector.

To borrow the adage that a rising tide lifts all boats, means that the inverse is also true. In a less supportive global economic environment with headwinds intensifying, domestic economic policy and reform has to do a lot more heavier lifting to support the economy. With a fragile global environment, a sluggish local economy, an outlook for the remainder of the year and into 2023 remaining uncertain and the prospects of things getting worse before improving now would be a good time to adopt a more frugal outlook.

Energy crisis is symptom of policy failure, and only reform will solve it

When analysing South Africa’s energy crisis, it is pointless to rehash how we got to this point. We know that the state ignored the warnings that electricity was running out, that maintenance was not done, that the grid has deteriorated to the point of near collapse, that corruption was allowed to run rampant and so on and so on ad-nauseam. What is needed now is focus on what can be done to finally begin addressing the problem.

The two most glaring issues that the energy supply industry (ESI) faces are the above-inflation-rate increases in electricity tariffs and the ever-present rounds of load-shedding due to the severe lack of capacity. We tend to equate the energy problem with Eskom but when viewing it from the broader ESI perspective and the roles played by the Department of Mineral Resources & Energy (DMRE), the National Energy Regulator of South Africa (Nersa), municipalities and the Independent Power Producers (IPPs), we see that Eskom is just one part of a much wider ecosystem and for things to get better we need more harmony between and among all these moving components.

South Africa has an energy shortfall of 4,000MW, according to the Council for Scientific and Industrial Research (CSIR), and this potentially represents a ready market for the private sector to invest in to the benefit of all.

As Eskom has stated repeatedly, it simply implements the policy set by the DMRE, it is the state, and only the state, that can facilitate the inclusion and participation of the private sector.

There are essentially two solutions to the crisis, which are not either/or options. One is what needs to be done in the immediate short term, the other what needs to be done in the longer term.

The immediate solution would be for the DMRE to put the 4000MW out for bid on Bid Window 7. The department has tended to cap how much capacity can be bid for but suppliers typically bid for more. In the last bid window 9,000MW were bid for – more than double the shortfall - most of it coming from renewable energy providers, however, the department only procured 2,583MW.

The Renewable Independent Power Producer Programme (REIPPP), which the DMRE developed in 2011, was intended to bring additional megawatts onto the grid through private-sector investment in wind, hydro and other sources of energy.

In April the DMRE called for proposals under Bid Window 6, which is looking to secure another 2,600MW of renewable energy (1,600MW of onshore wind and 1,000MW of solar photovoltaic) – approximately half of the 4,000MW shortfall.

The Integrated Resource Plan (IRP), which maps out South Africa’s energy demand and the least cost energy mix to meet that demand, while also charting a roadmap of South Africa’s planned transition from coal to cleaner energy sources as part of the international commitment to reduce greenhouse gases and decrease carbon emissions, has been criticised for being too soft on coal. But there are indications that the government is willing to revise it. Forestry, Fisheries and Environmental Affairs Minister Barbara Creecy told MPs in Parliament in March that Mineral Resources and Energy Minister Gwede Mantashe “has indicated to the climate commission that he is open to receiving presentations on revisions on the IRP, which obviously could be necessary if we are to achieve the lower limit of our nationally determined contribution (NDC)”. Given the rate at which renewable energy prices have dropped since 2011 and with the downward trajectory only anticipated to intensify, a much faster adoption of renewable energy projects has the potential to be environmentally friendly, while also limiting tariff inflation.

The longer-term solution is expediting the unbundling of Eskom to create an independent transmission company that will buy electricity from the market, including from state-owned Eskom and various IPPs, to sell to consumers. This ensures a bigger role for the private sector in the production of electricity, creating a competitive market that can make a real dent in tariff increases as well as increasing capacity, so that load-shedding eventually is phased out.

Eskom will play a smaller but still-relevant role – as one of the providers of electricity for the country, though it will need to improve its efficiency significantly to remain relevant and competitive.

There are five main benefits to this framework:

- Eskom is not killed off, but still has a role to play.

- Competition acts as a disciplining force on prices. We all want the cheapest energy, so players will need to keep up to date with new technologies to stay ahead of the pack and win over consumers.

- Customers can choose the type of energy they want; this is especially good news for companies that can reduce their carbon footprint by using only renewable energy and in turn allow their products to capture premiums on the international market.

- Companies can limit the penalties they have to pay on their products in certain regions for high-carbon usage. The EU, for example, has announced a carbon adjustment mechanism, where products will carry a penalty for high carbon usage, making them more expensive and therefore less competitive.

- The end user will benefit through market-determined tariffs and better-quality service.

Neither of these solutions are out of the realm of possibility and both would make big changes to the ESI, South Africa’s battle-scarred economy, our attractiveness to foreign investors and the everyday life of all South Africans.

But the reality is that the energy landscape is very much at the mercy of our elected politicians. It is unacceptable for South Africans to endure the current electricity crisis and ongoing bouts of loadshedding. Government needs to do and be seen to be doing everything in its power to ensure that this crisis, like state capture, becomes a thing of the past.

SEIFSA comments on the draft preferential procurement regulations (2022)

The Steel and Engineering Industries Federation of Southern Africa (SEIFSA) is the principal advocate for companies operating in the metals and engineering sector. SEIFSA as a federation represents 18 employer associations, who collectively represent in excess of 1100 companies. These companies employ 170 000 employees in the sector.

METALS AND ENGINEERING SECTOR FACT AND FIGURES

The metals and engineering sector constitutes 25.6% of the total manufacturing sector. The sector is an integral part of the global and domestic economy and a crucial supplier of inputs into sectors such as mining, the automotive sector, construction and other manufacturing industries.

| Sub-Sector | % of Manfacturing |

| Plastic products | 2,29 |

| Basic iron and steel products | 2,82 |

| Non-ferrous metal products | 3,26 |

| Structural metal products | 1,98 |

| Other fabricated metal products | 3,35 |

| General purpose machinery | 3,46 |

| Special purpose machinery | 3,87 |

| Household Appliances | 0,73 |

| Electrical machinery and apparatus | 2,31 |

| Bodies for motor vehicles, trailers and semi-trailers | 0,71 |

| Other transport equipment | 1,37 |

| Total M & E Sector | 26,15 |

Source: Statistics South Africa

The important facts and figures relating to the metals and engineering sector are contained below:

| Dashboard: Comparison of the 2020 to 2021, in the M&E Sector | ||

| ECONOMIC VARIABLE | 2020 | 2021 |

| M&E production (% growth) | -12,8% | 10,7% |

| M&E production sales (Rand value) | R633,6 billion | R804,1 billion |

| M&E capacity utilization (%) | 67,1% | 76,2% |

| M&E Employment (number) | 361 983 | 352 625 |

| Total M&E employment share (%) | 35,8% | 35,9% |

| M&E Export value (Rand billion) | R371, 3 billion | R458,8 billion |

| M&E Import value (Rand billion) | R432 billion | R531,5 billion |

| M&E Net trade balance (Rand value) | -R60,7 billion | -R72,7 billion |

| M&E Gross earnings (Rand current prices) | R104,5 billion | **R108,2 billion |

Source: Statistics South Africa, SARS, MIBFA

The graphs below are the most effective way of communicating the distress experienced in the sector. Production trends have been on a persistent downward trajectory since the 2008/9 global financial crisis from which the sector has never recovered. Naturally, the sector was not spared from the economic disruption of covid-19.

THE IMPORTANT ROLE OF THE STATE

State organs namely general government, state owned entities and the country’s 278 municipalities are key markets to which the metals and engineering sector supplies products. In 2020, state organs procurement amounted to R70.9 billion, or 22.9% of total domestic sales from the sector. Notably, state procurement from the electrical machinery sub-sector accounts for more than half (52%) of domestic sales. The importance of state procurement from the metals and engineering sector has necessitated that SEIFSA prepare this submission in response to the draft Preferential Procurement Regulations (2022) issued by the National Treasury for public comment. Public procurement has the potential to stimulate domestic demand for products from the metals and engineering sector, which will support economic and industrial development. State procurement is an important domestic demand anchor for the sector and contributes to facilitating greater economies of scale, which in turn contributes to competitiveness and export opportunities.

The conventional GDP equation (GDP = Consumption + Private-Investment + Government-Investment + (Exports – Imports) proposes that large scale private investment, which is inversely related to taxes and interest rates, drives economic growth. However, in reality private sector investment is also driven by “herd” instincts, which are naturally volatile and in turn makes the overall GDP outcome volatile. Greater domestic investment (and domestic procurement) by the state introduces a stable anchor on which the rest of the GDP components can be built on, thereby creating a stable and sustainable GDP trajectory, (Mariana Mazzucato - Entrepreneurial State, 2013).

Given the above context as a departure point and the importance of state procurement for the metals and engineering sector, SEIFSA submits that the draft preferential procurement regulations published by National Treasury run counter to the industrialisation aspirations of the country, have the potential to reverse the historic efforts that have been invested into processes of developing industry master plans and designation efforts. The regulations will also create an untenable environment wherein local companies will have to contend with multiple un-standardised procurement policies from different state organs.

The material aspects of SEIFSA’s submission to the draft Preferential Procurement Regulations (2022) are listed below:

- It is important to stress that SEIFSA’s concerns are not with the decision of the Supreme Court of Appeal (SCA) or the Constitutional Court on the Preferential Procurement Regulations. It is important that all regulations that direct the functioning of state organs are consistent with the country’s constitution. However, the concerns listed below relate to National Treasury’s interpretation of the court decision as inferred by the published draft Preferential Procurement Regulations 2022.

- The omission of local content, local production or designated products in the draft regulations, to give some preference to local companies from public procurement is a missed opportunity to leverage state procurement as an instrument to drive domestic industrialisation.

- To remove any forms of preference for domestic companies, in the absence of initially dealing with aspects that relate to the cost of doing business in the country is akin to putting the proverbial cart before the horse. The unfortunate outcome that is likely to manifest is that domestic companies will be unable to compete with imported products leading to further de-industrialisation. This is not to advocate that local procurement by the state and industrialisation should pursued at all costs and at the cost of competitiveness, however, the domestic input cost structures creates an unfavourable environment for companies to compete with imported products. The focus should be to create a suite of incentives from tax rates to industrial incentives that will assist domestic companies to compete if the preference for local procurement from domestic companies were to be removed.

- Efforts to revive the unprecedented levels of decline in the economic performance of the metals and engineering sector are contained in the Steel Master Plan (SMP), which is an industry initiative by government, labour and the private sector. The SMP envisages leveraging the country’s infrastructure drive and localisation by state owned entities as instruments to boost demand for locally produced products. The plan also proposes designation of locally produced products for public procurement as a stability measure that can be implemented in the short-term to support demand for local products. The draft preferential procurement regulations in the current form would in essence reverse all the efforts that have been invested by the sector in the development of the SMP. This point is possibly applicable to all the other sector master plans. This raises the very worrying prospect of inconsistent policy formulation in the state, where different national departments develop and pursue fundamentally different policy directions.

- In the absence of explicit regulations guiding state organs on the procurement policy, the Preferential Procurement Policy Framework Act (PPPFA) state that state organs will develop their own procurement policies based on socio-economic considerations listed in the Reconstruction and Development Programme (RDP) of 1994. This means that organs of state will develop their own measures for industrial, economic development and socio-economic aspirations. While these measures will support local economic development, SEIFSA submits that devolving this obligation to each state organ to create its own procurement policy will create an untenable administrative and compliance environment for domestic companies. It is paramount that National Treasury develops a national guideline for state organs to comply with in the development of their procurement policies. This will be important for institutional coordination and alignment across the multiple state organs. It will also make monitoring and enforcement of regulations possible. Coherence and uniformity should be the basis on which national regulations are developed.

- SEIFSA recommends that given the importance of these regulations and the possible unintended consequences that would manifest if they are to be passed in their current form, National Treasury should embark on an extensive consultation process in the development of these regulations. While it is acknowledged that regulations are an executive function that govern day-to-day functioning of the state, we submit that the policy implications of these regulations extend far beyond the aspects that they seek to regulate. As a result, SEIFSA recommends a thorough consultation process for these regulations be implemented through the NEDLAC processes. This will allow National Treasury the opportunity to receive much more detailed inputs from the social partners represented on the NEDLAC structures.

Thank you for the opportunity to make representation on behalf of the metals and engineering sector. We trust that our inputs will receive your favourable consideration.