SEIFSA delegation meets with Eskom

As part of SEIFSA’s lobbying and advocacy initiatives a delegation from SEIFSA comprising Senior Executives, CEOs and the Office (L Trentini and T Chibanguza, SEIFSA CEO and COO respectively), met with the Group Chief Executive Officer of Eskom, Mr Andre de Ruyter on the 25th of April 2022. In attendance from Eskom were Mr Monde Bala: Group Executive Distribution and Nkosana Ntlekeni: Key Accounts Executive Manager.

The objectives for requesting the meeting towards the end of 2021 had been to open a channel of communication and on-going dialogue with Eskom with a view to identifying strategic initiatives that SEIFSA on behalf of its affiliated membership and Eskom, can work on collaboratively in contributing to resolving the challenges experienced in the energy supply industry (ESI).

To this end, the following agenda points were submitted to Eskom in advance of the meeting in order to guide the discussion:

- Discussion on Eskom’s long term strategic vision and plans on the following:

- Maintenance (preventative and unplanned outages);

- Staff costs; and

- Cost of electricity (price path).

- Discussion on Eskom’s long-term plans on accelerating alternative energy sources onto the national grid.

- Discussion on the feasibility of by-passing municipalities and companies paying their electricity bill direct to Eskom.

- Ongoing and further collaboration between Eskom and SEIFSA

This brief note highlights some of the key aspects that emerged out of the meeting

- Eskom outlined the precarious state of the national grid and the origins of the current challenges, which include a lack of historic maintenance and delays to building new generation capacity. While building the Medupi and Kusile power stations, the organisation ran its generation capacity very hard, measured by the energy utilisation factor, while simultaneously neglecting maintenance. This, we were advised, has resulted in the long-term deterioration of the existing generation fleet. In addition, Eskom is struggling with on-going technical build problems at Medupi and Kusile, resulting in a situation where the power stations that were meant to relieve supply shortages cannot be fully relied on as yet, to ease the supply deficit.

- Maintenance is currently at 12%-13%, much lower than what Eskom would want it to be. However, a careful balance needs to be struck between planned maintenance and supplying electricity to the economy, against the backdrop of the poor state of the national grid.

- The limitations to resolving the challenges include, a lack of:

- money: to adequately finance the maintenance program to the extent that it is required;

- time: a lack of head-room from a generation capacity perspective to remove units from production while at the same time supplying electricity to the economy; and

- skills: which have been lost over the years constraining the ability for Eskom to resolve the challenges facing the organisation.

- Persistent and endemic corruption, which continues to plagues the organisation. This in itself was framed as one of the key constraints to resolving the challenges of the organisation.

Outlook

- Greater private sector investment into electricity generation capacity was identified as a key enabler to resolving the electricity supply challenge. Eskom does not see its future role as being one where it will be the primary source of new large scale generation capacity (its balance sheet simply does not permit this).

- The unbundling of Eskom with a dedicated transmission company that will act as a system market operator, to facilitate buying and selling of electricity between electricity producers and end customers is seen as a key enabler to bringing on private sector investment. Eskom indicated that it is in the process of setting up the electricity trading platform.

- It was mentioned that the electricity tariffs that could potentially be achieved through this trading platform could be market determined, which would go a long-way towards controlling the pace and extent of tariff increases into the future.

- Eskom indicated that these unfolding processes will open business opportunities in the economy. Eskom intends to retire 22 GW of coal fired generation capacity by 2035. This, it was stressed, will presents opportunities to convert this capacity to gas, an important enabler toward a just energy transition. Greater solar and wind capacity will also need to be developed to compensate for retired coal capacity. The metals and engineering sector it was mentioned could set to benefit from these developments, along with other sectors of the economy.

- Eskom will be embarking on an 8000 km build program to strengthen and grow the transmission network to allow independent power producers access to the grid, would again presents opportunities for the sector and the economy.

Areas of collaboration between Eskom and SEIFSA

- On the opportunities that are unfolding from the developments in the electricity supply industry, a significant amount of effort needs to be invested in policy formulation on how the country can take full advantage of these opportunities. Localisation, local content, industry development incentives, designation, etc., will need to be explored further to determine decisions that are in the best interest of the sector and the greater economy.

- Eskom indicated a clear willingness to work with SEIFSA, representing its affiliated membership on these and other matters. This is an important development due to the potential cost implications for Eskom, whilst presenting opportunities to develop nascent industries within the sector and the country.

- Municipal debt was identified as a massive problem for Eskom (currently growing at R 7.3 billion per annum). Eskom has indicated that organised business organisations should be more involved in aspects relating to municipalities. SEIFSA on behalf of its affiliated membership, Eskom stressed, could play an important role in this regard, given the vast geographical spread of its members across the country’s multiple municipalities.

- Eskom indicated a willingness to further explore models of direct supply and payment between Eskom and end customers, however, Eskom stressed that any considerations in this regard need to take into account the sustainability of the municipalities. Eskom highlighted that every geographical area of the country is covered by a municipality, and therefore it would be ill-advised to pursue decisions that undermine the sustainability of the municipalities.

- Grid Access Unit (GAU): Eskom has set up a unit that manages aspects relating to accessing the national electricity grid. Regulated bids, which are facilitated through the Renewable Independent Power Producer Programme (REIPPP), we were advised are now much easier to manage. The challenge faced by the GAU is with unregulated bids, where companies build capacity behind the meter or on a bilateral basis between a customer and IPP. Eskom. Indicated its willingness to work with SEIFSA in consolidating the unregulated bids within the metals and engineering sector.

- Theft and vandalism of Eskom’s infrastructure was highlighted as amounting to a major problematic area that Eskom continues to dealing with. Eskom suggested that SEIFSA and its membership should consider working with Eskom in the following areas:

- the development of the specifications of electricity cables to make them less attractive to cable theft; and/or

- advocating for improving scrap metal regulations to eliminate unscrupulous operators while allowing legitimate businesses to continue to operate.

In closing, the president has been emphasising the importance of attracting investment to SA to boost economic growth. The crisis at Eskom can only diminish the confidence of potential external investors in our economy if they cannot be guaranteed a stable and predictable supply of power.

The parting impression gleamed from today’s session is that the Eskom Group CEO and his Team appear to have the determination to continue to do what must be done, no matter how unpopular. This will unfortunately result in more not less rotational power cuts in the short term hopefully resulting in noticeable improvements in the medium term.

What is not in dispute is Eskom’s position within the SA economy, it is so pivotal that it cannot be allowed to collapse. Power stations will be taken down and maintained for longer than has been the case in the past, new renewable energy capacity must be brought on stream quicker and those responsible for corruption must be rooted out.

SEIFSA on behalf of the affiliated membership looks forward to playing its part.

Steel Master Plan needs industry’s commitment to take flight

Almost a year after the launch of the Steel Master Plan (SMP), Scaw Metals CEO Doron Barnes acknowledges the frustration many in the industry feel about the Plan, but he also believes it has the potential to rejuvenate upstream and downstream industries.

Much of the criticism of the plan is a result of a misunderstanding of its role, he said.

The Plan — which was launched on June 11 2021 and signed by representatives of Government, Business and Labour — provides a series of practical steps for the steel and engineering industry to follow in order to reinvigorate itself.

The Steel and Engineering Federation of Southern Africa (SEIFSA) will give everyone a chance to discuss their frustration, praise and ask questions about the Plan at the Mainstreaming the Steel Master Plan Conference on May 19 and 20.

Like Barnes, Macsteel CEO Mike Benfield also has strong views about the Plan. “We need to re-energise it, we need to prioritise and we need to get workstreams going around those priorities,” he says. He is concerned that it will not become a reality without a whole-hearted commitment to a list of prioritised infrastructure projects, specifically in the areas of rail, ports and power.

Barnes, in a recent interview with Creamer Media Engineering News & Mining Weekly, is adamant that industry must take the lead. “It is up to industry to take leadership by dedicating time, energy and resources to make it work, rather than sitting back and moaning about all the problems.”

SEIFSA CEO Lucio Trentini agrees with this, saying: “This industry stands ready to make its contribution to translating the government’s vision of reindustrialising the metals and engineering (M&E) sector, and to start translating visions, promises and policy into action and deliverables.”

“We need government to roll-out its promised infrastructure spend, which is absolutely central to the reigniting of industrial capacity in the sector.”

SEIFSA is eager to see many small business owners at the conference. “We urge SMEs to attend the conference so their important voices can also be heard. It is crucial that they too are well represented at the conference” says Trentini.

Large corporates, SMEs, company executives, public servants and anyone keen to find out more can visit the conference website (https://www.seifsa.co.za/product/steel-master-plan-conference/) for all the details of the Mainstreaming the Steel Master Plan conference.

The conference will play host to senior Department of Trade, Industry and Competition officials, representatives from the Steel Oversight Committee, Business and Labour leaders who will analyse the progress of the plans as well as the commitments that will lay the foundations for the development and growth of the M&E sector in the years ahead.

Minister of Trade, Industry and Competition Ebrahim Patel will deliver the keynote address, after an opening address from Elias Monage, SEIFSA President. Other speakers include Irvin Jim, the General Secretary of National Union of Metalworkers of South Africa (NUMSA), and Marius Croukamp, Deputy General Secretary of Solidarity.

There will also be a series of panel discussions looking at supply-side measures, demand-side measures, transformation, resource mobilisation and the African Continental Free Trade Agreement.

Trentini said: “The big gains will be made by moving our infrastructure programme from shallow waters to deep waters and to get it moving on a bigger scale and then introducing a localisation requirement not only on primary steel, but also downstream steel.”

The Mainstreaming the Steel Master Plan conference will be held on May 19 and 20 at Industrial Development Corporation, Sandton.

The conference will be organised and hosted by SEIFSA in partnership with the Industrial Development Corporation and the Department of Trade, Industry and Competition.

SEIFSA comments on the draft preferential procurement regulations (2022)

The Steel and Engineering Industries Federation of Southern Africa (SEIFSA) is the principal advocate for companies operating in the metals and engineering sector. SEIFSA as a federation represents 18 employer associations, who collectively represent in excess of 1100 companies. These companies employ 170 000 employees in the sector.

METALS AND ENGINEERING SECTOR FACT AND FIGURES

The metals and engineering sector constitutes 25.6% of the total manufacturing sector. The sector is an integral part of the global and domestic economy and a crucial supplier of inputs into sectors such as mining, the automotive sector, construction and other manufacturing industries.

| Sub-Sector | % of Manfacturing |

| Plastic products | 2,29 |

| Basic iron and steel products | 2,82 |

| Non-ferrous metal products | 3,26 |

| Structural metal products | 1,98 |

| Other fabricated metal products | 3,35 |

| General purpose machinery | 3,46 |

| Special purpose machinery | 3,87 |

| Household Appliances | 0,73 |

| Electrical machinery and apparatus | 2,31 |

| Bodies for motor vehicles, trailers and semi-trailers | 0,71 |

| Other transport equipment | 1,37 |

| Total M & E Sector | 26,15 |

Source: Statistics South Africa

The important facts and figures relating to the metals and engineering sector are contained below:

| Dashboard: Comparison of the 2020 to 2021, in the M&E Sector | ||

| ECONOMIC VARIABLE | 2020 | 2021 |

| M&E production (% growth) | -12,8% | 10,7% |

| M&E production sales (Rand value) | R633,6 billion | R804,1 billion |

| M&E capacity utilization (%) | 67,1% | 76,2% |

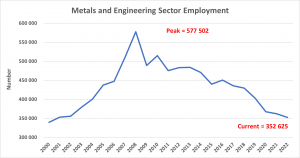

| M&E Employment (number) | 361 983 | 352 625 |

| Total M&E employment share (%) | 35,8% | 35,9% |

| M&E Export value (Rand billion) | R371, 3 billion | R458,8 billion |

| M&E Import value (Rand billion) | R432 billion | R531,5 billion |

| M&E Net trade balance (Rand value) | -R60,7 billion | -R72,7 billion |

| M&E Gross earnings (Rand current prices) | R104,5 billion | **R108,2 billion |

Source: Statistics South Africa, SARS, MIBFA

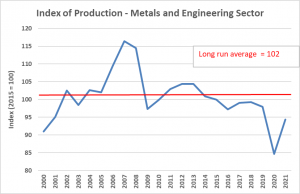

The graphs below are the most effective way of communicating the distress experienced in the sector. Production trends have been on a persistent downward trajectory since the 2008/9 global financial crisis from which the sector has never recovered. Naturally, the sector was not spared from the economic disruption of covid-19.

THE IMPORTANT ROLE OF THE STATE

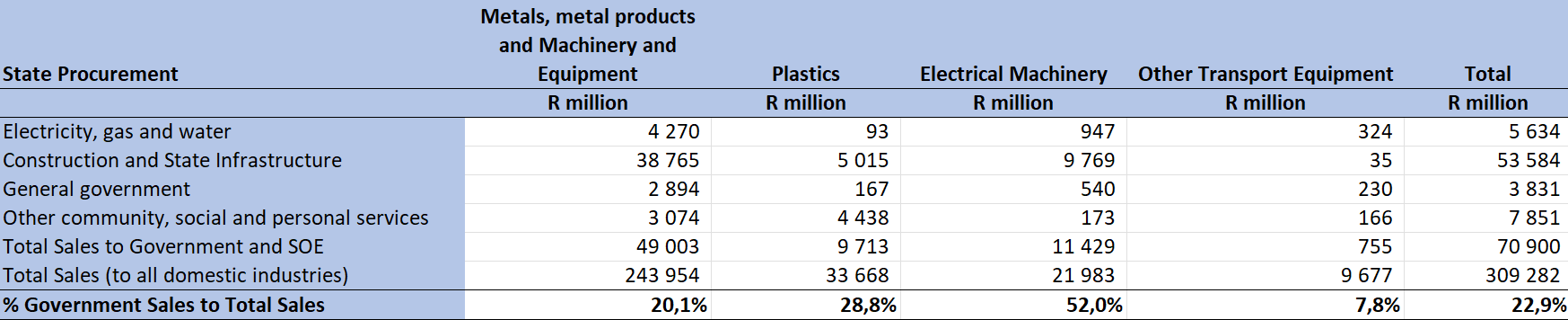

State organs namely general government, state owned entities and the country’s 278 municipalities are key markets to which the metals and engineering sector supplies products. In 2020, state organs procurement amounted to R70.9 billion, or 22.9% of total domestic sales from the sector. Notably, state procurement from the electrical machinery sub-sector accounts for more than half (52%) of domestic sales. The importance of state procurement from the metals and engineering sector has necessitated that SEIFSA prepare this submission in response to the draft Preferential Procurement Regulations (2022) issued by the National Treasury for public comment. Public procurement has the potential to stimulate domestic demand for products from the metals and engineering sector, which will support economic and industrial development. State procurement is an important domestic demand anchor for the sector and contributes to facilitating greater economies of scale, which in turn contributes to competitiveness and export opportunities.

The conventional GDP equation (GDP = Consumption + Private-Investment + Government-Investment + (Exports – Imports) proposes that large scale private investment, which is inversely related to taxes and interest rates, drives economic growth. However, in reality private sector investment is also driven by “herd” instincts, which are naturally volatile and in turn makes the overall GDP outcome volatile. Greater domestic investment (and domestic procurement) by the state introduces a stable anchor on which the rest of the GDP components can be built on, thereby creating a stable and sustainable GDP trajectory, (Mariana Mazzucato - Entrepreneurial State, 2013).

Given the above context as a departure point and the importance of state procurement for the metals and engineering sector, SEIFSA submits that the draft preferential procurement regulations published by National Treasury run counter to the industrialisation aspirations of the country, have the potential to reverse the historic efforts that have been invested into processes of developing industry master plans and designation efforts. The regulations will also create an untenable environment wherein local companies will have to contend with multiple un-standardised procurement policies from different state organs.

The material aspects of SEIFSA’s submission to the draft Preferential Procurement Regulations (2022) are listed below:

- It is important to stress that SEIFSA’s concerns are not with the decision of the Supreme Court of Appeal (SCA) or the Constitutional Court on the Preferential Procurement Regulations. It is important that all regulations that direct the functioning of state organs are consistent with the country’s constitution. However, the concerns listed below relate to National Treasury’s interpretation of the court decision as inferred by the published draft Preferential Procurement Regulations 2022.

- The omission of local content, local production or designated products in the draft regulations, to give some preference to local companies from public procurement is a missed opportunity to leverage state procurement as an instrument to drive domestic industrialisation.

- To remove any forms of preference for domestic companies, in the absence of initially dealing with aspects that relate to the cost of doing business in the country is akin to putting the proverbial cart before the horse. The unfortunate outcome that is likely to manifest is that domestic companies will be unable to compete with imported products leading to further de-industrialisation. This is not to advocate that local procurement by the state and industrialisation should pursued at all costs and at the cost of competitiveness, however, the domestic input cost structures creates an unfavourable environment for companies to compete with imported products. The focus should be to create a suite of incentives from tax rates to industrial incentives that will assist domestic companies to compete if the preference for local procurement from domestic companies were to be removed.

- Efforts to revive the unprecedented levels of decline in the economic performance of the metals and engineering sector are contained in the Steel Master Plan (SMP), which is an industry initiative by government, labour and the private sector. The SMP envisages leveraging the country’s infrastructure drive and localisation by state owned entities as instruments to boost demand for locally produced products. The plan also proposes designation of locally produced products for public procurement as a stability measure that can be implemented in the short-term to support demand for local products. The draft preferential procurement regulations in the current form would in essence reverse all the efforts that have been invested by the sector in the development of the SMP. This point is possibly applicable to all the other sector master plans. This raises the very worrying prospect of inconsistent policy formulation in the state, where different national departments develop and pursue fundamentally different policy directions.

- In the absence of explicit regulations guiding state organs on the procurement policy, the Preferential Procurement Policy Framework Act (PPPFA) state that state organs will develop their own procurement policies based on socio-economic considerations listed in the Reconstruction and Development Programme (RDP) of 1994. This means that organs of state will develop their own measures for industrial, economic development and socio-economic aspirations. While these measures will support local economic development, SEIFSA submits that devolving this obligation to each state organ to create its own procurement policy will create an untenable administrative and compliance environment for domestic companies. It is paramount that National Treasury develops a national guideline for state organs to comply with in the development of their procurement policies. This will be important for institutional coordination and alignment across the multiple state organs. It will also make monitoring and enforcement of regulations possible. Coherence and uniformity should be the basis on which national regulations are developed.

- SEIFSA recommends that given the importance of these regulations and the possible unintended consequences that would manifest if they are to be passed in their current form, National Treasury should embark on an extensive consultation process in the development of these regulations. While it is acknowledged that regulations are an executive function that govern day-to-day functioning of the state, we submit that the policy implications of these regulations extend far beyond the aspects that they seek to regulate. As a result, SEIFSA recommends a thorough consultation process for these regulations be implemented through the NEDLAC processes. This will allow National Treasury the opportunity to receive much more detailed inputs from the social partners represented on the NEDLAC structures.

Thank you for the opportunity to make representation on behalf of the metals and engineering sector. We trust that our inputs will receive your favourable consideration.

Paid holidays for the metal industry

With the long weekend coming up, many companies will be wondering how to apply and interpret the Public Holiday provisions in the Main Agreement. In this article, prepared by SEIFSA’s Industrial Relations Division, the application of Public Holidays is clarified.

All the Public Holidays specified in the Public Holidays Act are paid holidays for employees covered by the Main Agreement.

Employees covered by the Agreement are not required to work on a Public Holiday and are entitled to full pay if the day falls on an ordinary working day. Companies working a Monday to Friday work week are not required to pay employees for a Public Holiday if it falls on a non-working day, for example Saturday (24 September 2022) unless employees work on that day.

Working on a paid Public Holiday

Where an employee works on a paid Public Holiday the employee is entitled to:

- The rate of pay for an ordinary shift; plus

- One-and-a-third times the hourly rate for the hours worked.

If an employee works overtime i.e., hours in excess of the normal hours on that day, then he/she is entitled to an additional two-and-a-half times the hourly rate for those extra or overtime hours.

Where a Public Holiday falls on a Sunday

Public Holiday’s falling on a Sunday will be observed as a paid public holiday the following Monday. Employees who are called-in to work on a Sunday, which happens to be a Public Holiday, will be paid at Sunday rates i.e., double-time.

The one exception to this rule is where Christmas Day falls on a Sunday. Employees working on Christmas Day, which happens to be a Public Holiday, will be paid at the Public Holiday rate. This is due to the next day being Day of Goodwill.

Paid Public Holidays and shift workers

Difficulty often occurs where employees work a two or three-shift system, especially where part of the shift falls on the Public Holiday. In such a case, the worker will be paid for the shift before, during or after their shift as if it were a paid Public Holiday. Therefore, the whole shift, if not worked through the Public Holiday, irrespective of where it falls, will be paid on Public Holiday rates. Where the employee works overtime on that particular shift, they must be paid at two-and-a-half times for the overtime hours.

For example, a night-shift employee starts his shift at, say 18:00 on Thursday, 15 June 2022 and ends his shift on Friday, 16 June 2022. The part of the shift from midnight onwards falls on the Public Holiday. If the employee’s next shift starts at 18:00 on 16 June 2022, the option is to treat either the whole shift starting on 15 June or the whole shift starting on 16 June 2022 as the public holiday.

Annual leave and Public Holidays

If a Public Holiday falls within an employee’s annual leave on a day which would have been a normal working day, then the leave period must be extended by one day with full pay for the day. Where Public Holiday’s fall on a non-working day then the annual leave is not extended.

Public Holiday during periods of short-time or lay-off

Any Public Holiday during a period of short-time or lay-off must be regarded as falling on an ordinary working day, and the employee must be paid at the ordinary hourly rate for that day.

Work-in-time arrangements to extend Public Holidays

Management and employees may agree to work time in, so that designated normal working days may be treated as paid holidays, thereby extending existing public holidays and creating long weekends. For example, 16 June 2022 falls on Thursday. The workforce may work on an elected non-working a such as a Saturday, in return for a paid holiday on Friday 17 June 2022. Requirements to implement this arrangement are management support, a 75 percent positive ballot amongst the workforce and an exemption from the Council.

Absence after or before a Public Holiday

Where an employee is absent the day before or the day after a Public Holiday, the employee does not lose his/her entitlement to be paid for the public holiday. However, this does not absolve him/her from appropriate disciplinary action if the reasons for the absence do not validate his/her absence.

Where management requires further assistance, they should contact SEIFSA’s Industrial Relations Division (011) 298-9400.

Save the date for SEIFSA's Mainstreaming the Steel Master Plan Conference

The Steel and Engineering Federation of Southern Africa (SEIFSA) will give Government, Business and Labour a chance to assess the progress of the Steel Master Plan (SMP) at its Mainstreaming the Steel Master Plan Conference on May 19 and 20.

The Plan — which was launched on June 11 2021 and signed by representatives of Government, Business and Labour — provides a series of practical steps for the steel and engineering industry to follow in order to reinvigorate itself.

Almost one year after the plan was signed, the industry is ready to see it take shape. SEIFSA CEO Lucio Trentini said: “This industry stands ready to make its contribution to translating the government’s vision of reindustrialising the metals and engineering (M&E) sector, and to start translating visions, promises and policy into action and deliverables.”

“We need government to roll-out its promised infrastructure spend, which is absolutely central to the reigniting of industrial capacity in the sector.”

The steel industry, as a direct driver of growth, investment and jobs, and as indirect supporter of the construction, automotive and mining sectors, is a crucial component in boosting the country’s industrial capacity.

“It’s going to be about increasing domestic demand for steel,” Minister of Trade, Industry and Competition Ebrahim Patel said at the signing of the Steel Master Plan.

The conference will play host to senior Department of Trade, Industry and Competition officials, representatives from the Steel Oversight Committee, Business and Labour leaders who will analyse the progress of the plans as well as the commitments that will lay the foundations for the development and growth of the M&E sector in the years ahead.

Minister of Trade, Industry and Competition Ebrahim Patel will deliver the keynote address, after an opening address from Elias Monage, SEIFSA President. Other speakers include Irvin Jim, the General Secretary of National Union of Metalworkers of South Africa (NUMSA), and Marius Croukamp, Deputy General Secretary of Solidarity.

There will also be a series of panel discussions looking at supply-side measures, demand-side measures, transformation, resource mobilisation and the African Continental Free Trade Agreement.

Trentini said: “The big gains will be made by moving our infrastructure programme from shallow waters to deep waters and to get it moving on a bigger scale and then introducing a localisation requirement not only on primary steel, but also downstream steel.”

The Mainstreaming the Steel Master Plan conference will be held on May 19 and 20 at Industrial Development Corporation, Sandton.

The conference will be organised and hosted by SEIFSA in partnership with the Industrial Development Corporation and the Department of Trade, Industry and Competition.