Temporary Employment Services (TES)

The Metal Industry Main Agreement (MA) was gazetted by the Minister of Employment and Labour on 7 October and became legally binding on all employers, including Temporary Employment Service (TES) providers, in the metals and engineering (M&E) sector on 17 October 2022.

A key and unique feature of the MA is that it does not differentiate between an employer owning and/or overseeing a factory and a TES provider providing labour and related services to employers in the sector. The MA treats both exactly the same and apart from the provisions related to joint and several liability contained in the Labour Relations Act (LRA), TES providers in a post gazettal operating environment are legally obliged to adhere to all the terms and conditions of engagement, employment and deployment contained in the MA.

Over and above what the LRA prescribes for TES providers, the MA sets out a comprehensive set of terms and conditions related to how TES providers should operate in the M&E sector. In a post gazettal environment, should must be read as shall and whilst some TES providers may be tempted to cut corners and claim ignorance when it comes to various legal compliance obligations contained in the MA, the Bargaining Council i.e., the industry’s compliance and enforcement agency, will not be swayed by arguments of ‘’I did not know” or “I wasn’t aware”.

Clients of TES providers who knowingly or unknowingly enter into commercial agreements containing provisions in conflict with the MA will be found wanting. The Bargaining Council will have no hesitation in following up on such complaints, will site the TES provider and the client in any ensuing dispute and should the client and/or the TES provider be found wanting, joint and several liability will come into play.

In a business environment where legal compliance is becoming increasingly complicated, it’s imperative when considering making use of a TES provider, you do so knowing you are contracting with an agency that is reputable, compliant and most importantly, has been vetted by a body that was instrumental in getting TES providers recognized as being no different to any other employer operating in the M&E sector – the CEA (TESD).

The Temporary Employment Services Division of the CEA is the only reputable voluntary professional body of TES providers in the M&E sector. The body speaks for and on behalf of TES providers and ensures that TES providers are treated no different to any other employer in the sector, are recognized for the important service they provide and are acknowledged for the many thousands of pathways they have created for employees who have been provided to clients and over time find permanent employment.

The CEA (TESD), as a condition of accredited membership, will require that a TES provider seeking affiliation subject itself to an accreditation audit , conducted by an independent auditor, appointed by the CEA (TESD) in order to verify and validate legal compliance with provisions contained in the MA, LRA, MEIBC, MIBFA etc. Having passed the audit, the TES provider will be issued with a certificate of compliance and will be loaded to the industry data base of compliant TES providers. This process enjoys the full support of the Bargaining Council, the Department of Employment and Labour, industry trade unions and for employers or clients amounts to a resounding vote of confidence and peace of mind.

Should you be interested in joining a body of reputable and professional TES providers and in the process network and be part of the on-going discussions related to the future of TES providers in the metals and engineering industry, no more than ever would be a good time to do so.

To join the CEA (TESD) or to get more information on the benefits of being a member email Christa Smith at christa@associationadministrator.co.za or visit the TESD website at www.tesd.org.za.

SEIFSA load shedding impact assessment on the Metals and Engineering Sector

The energy crisis that is gripping South Africa presents the most significant risk and binding constraint to the economic prospects of the country. The crisis not only has implications on the immediate survival of companies but also on the long-term implications regarding the investment prospects of the country. The crisis has been particularly damaging on the metals and engineering sector, a sector which is the backbone of industrialisation and to which electricity, particularly baseload electricity, is fundamental to its survival.

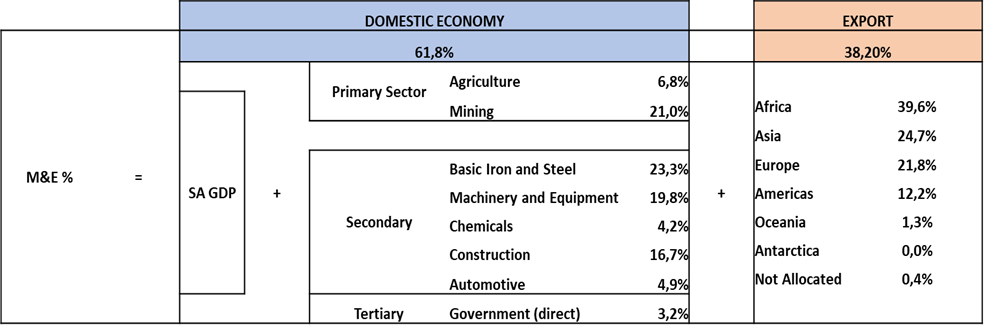

SEIFSA represents 18 Employer Associations, who collectively represent in excess of 1 300 companies and employ in excess of 170 000 employees in the metals and engineering (M&E) sector. The M&E sector constitutes 26.5% of the manufacturing sector, based on output, and 2.6% the country’s gross domestic product (GDP) on a value-add basis. As at December 2022 the sector employed 374 496 (of which 217 618 are factory workers) who are employed in approximately 10 00 companies.

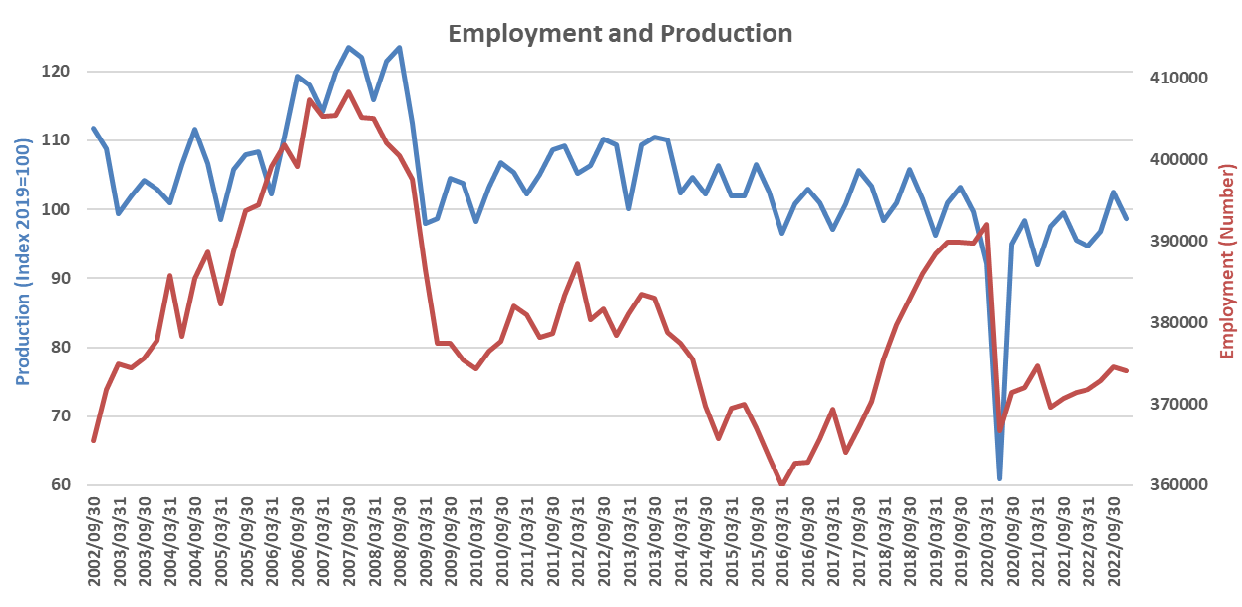

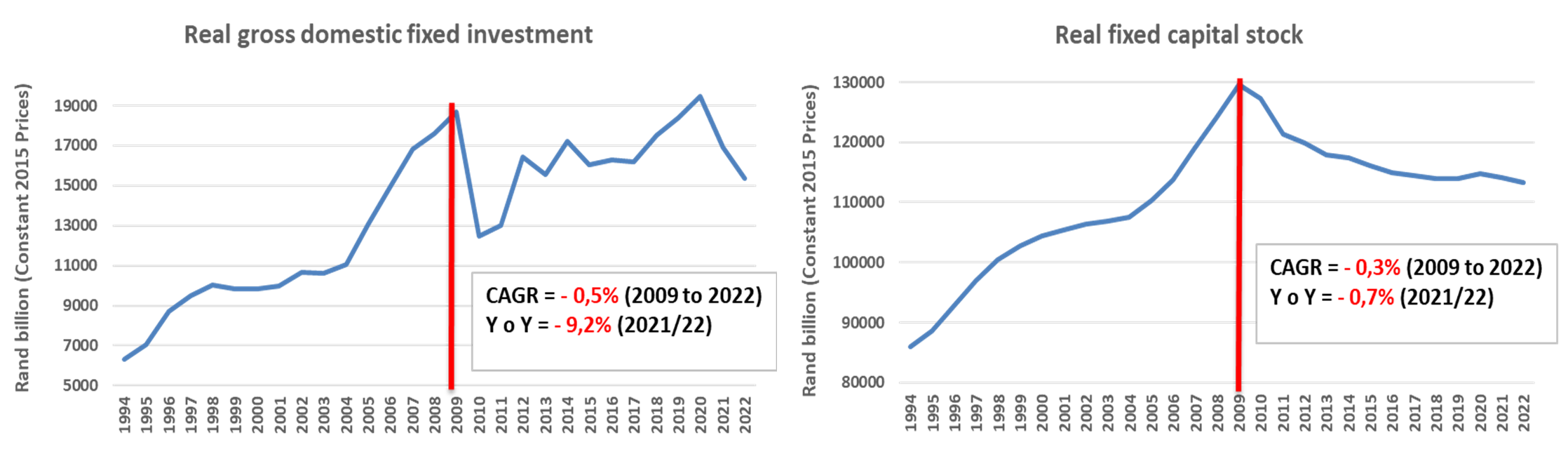

It is important to highlight, in brief, the historic context in which this survey is conducted. The M&E sector has been in a structural recession since the global financial crisis of 2008/9, with production recording a 1.2% contraction on a compound annual basis over this 15-year period. Given the less supportive global economic environment and the impact of domestic rigidities, chiefly the energy crisis, production in the sector is expected to contract further by 2.2% in 2023. Unfortunately, employment in the sector has also mirrored the production trends contracting at -1.1% (CAGR) and contributing to the country’s unemployment crisis. These trends are contained in the graph below. The Covid-19 induced lockdowns presented a major economic shock to the sector and although the production levels recovered (still 1% below pre-covid levels), employment trends have not (4.6% below pre-covid levels). Increasingly the sector has observed a weakening relationship between production and employment, meaning improving production outcomes are no longer a necessary condition for employment creation.

Source: SEIFSA, Statistics South Africa

The intensifying electricity crisis now presents the most prevalent economic risk to the sector:

It is in this context that SEIFSA undertook to survey its affiliated membership and developed this load-shedding impact assessment. This survey measures the impact of the energy crisis over a 12-month period (February 2022 to February 2023) across four main parameters, namely:

1. Employment;

2. Production;

3. Investment;

4. An analysis of the alternative energy investments made by the sector; and

5. Impact to Input costs.

The survey garnered a positive response, with 206 companies responding. The survey parameters are included below:

| Category | Survey Sample |

| Number of respondents (companies) | 206 |

| Total Employee Count (from responding companies) | 37 284 |

| Average number of employees (proxy for company size) | 184 |

| % of sample to total SEIFSA member employee headcount | 26.5% |

| % of sample to total M&E Sector employee headcount | 9.9% |

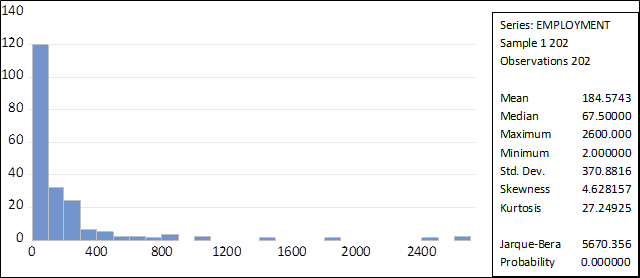

The employee headcount is the pivot variable for the purposes of consolidating the statistics, particularly the weighted outcomes. The companies that responded to the survey vary in head count from 2 employees to 2600 employees.

The straight average headcount across the sample is 184 employees yielding a good mix between large, medium and small companies. The definition of small to medium companies in the sector, based on headcount, is 50 employees or less. These companies represent 41.3% of the sample. The histogram below indicates the distribution of the company sizes relative to employment:

The consolidated results of the survey are contained in the table on the next page.

It is necessary to bear in mind that these results are from a sample representing 10% of the sector (measured on an employment metric).

Theoretically, the outcomes, particularly the absolute numbers, could be multiplied by 10 to get the full impact on the sector.

Consolidated results of the survey:

Employment:

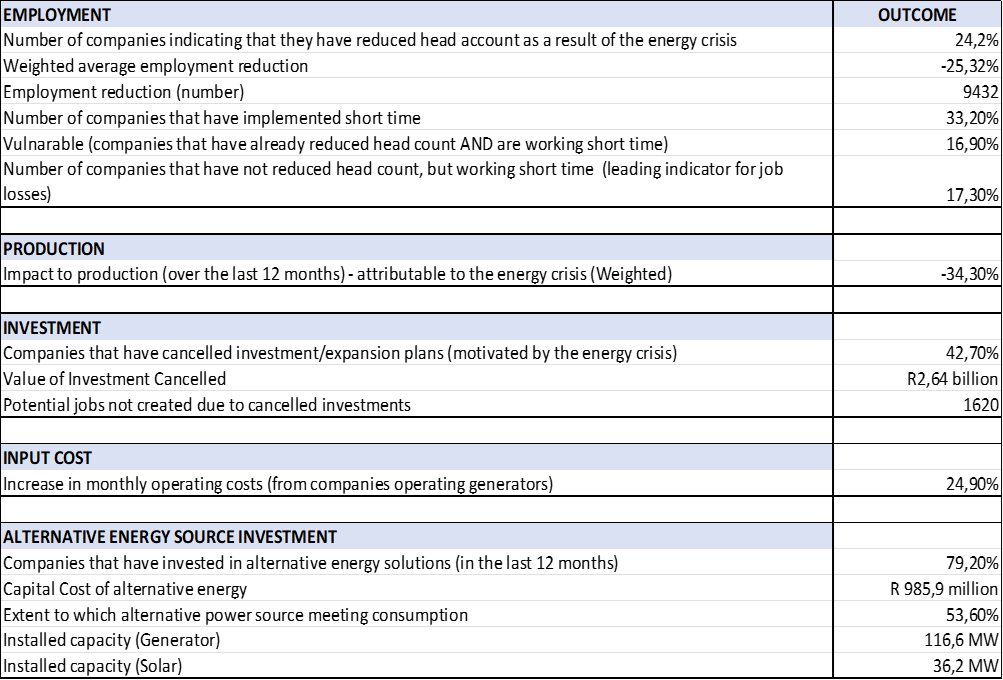

• The employment losses, mostly attributable to companies responding to the energy crisis over the reference period, indicate some very concerning trends.

• A quarter of companies indicated that they have had to reduce head count in response to the electricity crisis, by as much as a quarter of their employment, equating to 9 432 people.

• A third of the sample indicated that they are working short-time due to the electricity crisis.

• An even more concerning outcome is the fact that half (16.9%) of those companies that are implementing short time have already reduced head count.

• We assign the status of “vulnerable” to these companies, while the other half (17.3%) have not reduced head count, however, short time is a good leading indicator to track for potential future job losses.

Production:

• The respondents to the survey indicated production declines as much as 34.2% (weighted) as a result of the electricity crisis.

• Based on the model in the table below, SEIFSA has calculated that production in the sector is estimated to contract by 2.2% in 2023.

• However, factoring in the results from this survey, the forecast for the 2023 year deteriorates to – 5.3% for the 2023 year.

Investment:

• The long-term implications of this energy crisis to the future prospects of the sector are devastating.

• Over the last 15 years, net-investment into the sector has been on the decline, which has led to the value of fixed capital stock deteriorating at -0.3% (CAGR), threatening the competitiveness of the sector.

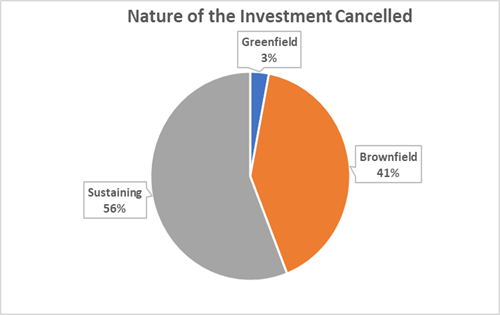

• It is therefore concerning that 42.6% of companies have indicated that they have cancelled investment and/or expansion plans owing to the uncertainty presented by the electricity crisis.

• The value of these investments amounts to R2.64 billion with the potential of creating 1 620 new jobs. The split of the nature of investment is included below.

An analysis of the alternative energy investments made by the sector:

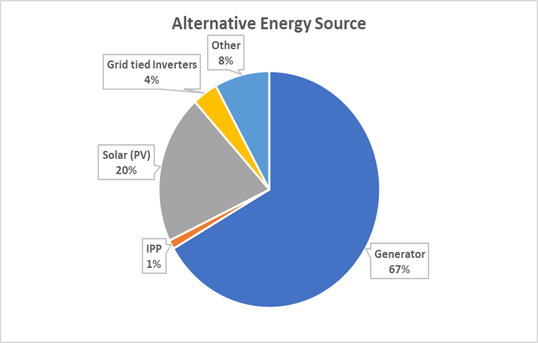

• 79.2% of companies indicated that they have had to install alternative electricity sources in the last 12 months to counter the pressing challenge presented by the electricity crisis.

• The combined value of this investment is R985 million. This number if considerable when considering that it accounts for 37% of the value of investments cancelled. This again highlights the point that SEIFSA has repeatedly stressed that companies are sacrificing scarce long-term capital to fulfil an immediate survival, presenting long-term adverse implications regarding the sustainability of the sector.

• The breakdown of the alternative technology source invested into is contained in the pie chart below. It is not surprising that given the relatively intense electricity consumption nature of the sector, the most practical alternative energy sources are generators representing 67%.

• Solar accounts for 20% of the investment made. It should however be borne in mind that this survey was done prior to the announcement of the 125% tax incentive afforded to companies in the February 2023 National Budget. This incentive should result in an increase in the up-take of solar an alternative source, however, the electricity consumption profile of the sector remains a limitation to solar being a full-scale option.

• On aggregate the companies have a generator installed capacity of 116MW, while that of solar is 36.2%.

• The respondents have registered very limited ability to feed-in any excess electricity generated from their solar installations, largely because of the fact that the solar installations have been put in as a marginal hedge or top-up to their baseload needs. This picture may well change given the 125% tax incentive, although to a limited degree, because the sectors electricity consumption pattern is the main determinant for the technology deployed.

Input Costs:

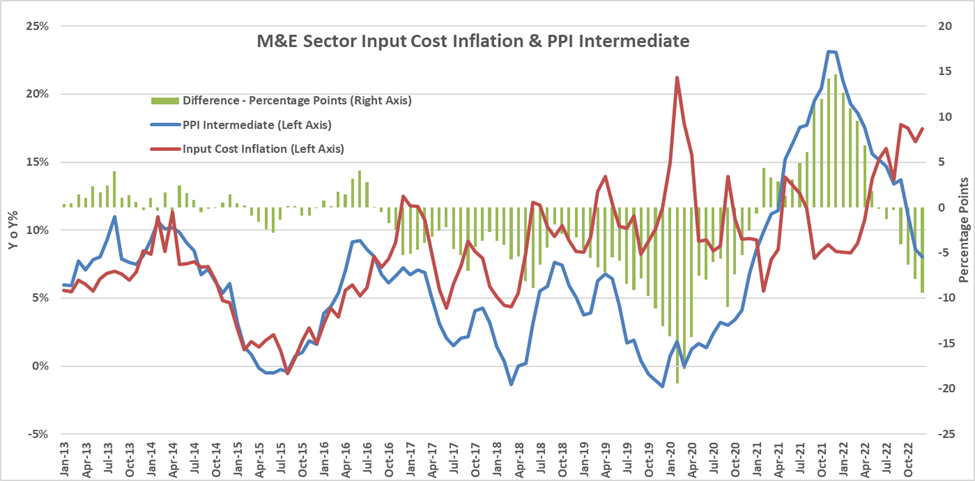

• On a weighted average basis, companies have indicated increases to monthly operating costs to the extent of 24.9% from the extensive use of generators.

• This does not bode well for a sector whose input costs are running at 17.6% (y o y - February 2023).

• Factoring in the results of the survey to the input cost model results in input costs increasing by 1.7 percentage points to 19.3% for the sector.

• The less supportive demand environment means that these companies cannot easily pass on these costs, thereby resulting in considerable margin squeeze and ultimately long-term sustainability.

We would like to thank the SEIFSA affiliated membership who have taken the time to complete this load shedding impact assessment survey.

The results of the survey are extremely valuable in providing tangible and quantifiable results which are necessary in various engagements SEIFSA will be having with key stakeholders responsible for resolving South Africa’s gripping electricity crisis.

Fixing industry: NEASA, get off the rooftops and into the ring

When the President made the call to business to ‘’get off the rooftops’’ and ‘’into the ring’’ to play its part in addressing crippling issues related to energy, logistics and crime to name a few – SEIFSA headed the call and continues to bring its capacity and resources to bear in addressing these and many other crises.

SEIFSA has consistently indicated its readiness to work with all stakeholders including government to shift the needle in putting our country onto a sustainable and inclusive growth path. We will, on the basis of such indications, continue to work with all stakeholders and not shy away from holding stakeholders to account as we act with urgency to rebuild trust amongst all social partners.

Conspicuously absent in all these engagements, apart from the periodic Newsletter, has been the voice of NEASA. In its own eyes, NEASA has a special understanding of the dynamics of the metals and engineering industries. Its boring refrain is both simple and simplistic: “All our economic pain comes from SEIFSA.’’ There is little wonder, then, that when one objectively surveys more than twenty years of NEASA’s participation on the Metals and Engineering Industries Bargaining Council, the only unbroken thread that can be discerned from its participation is its extraordinary and spectacular record of not having achieved a single thing for its constituency.

Times are tough in the country now, so many of the problems closing businesses and killing jobs could have been avoided. In these times, what can those of us mandated to act for business do? We are entitled and have every right to be angry and we should express it, but in ways that provides energy for action rather than draining us. Constructive criticism, engagement and action can make a difference, especially if we express our message in a way that models what we want to see.

It's easy to criticize, to engage in penny-pinching and throw barbs, but doing so without advancing any reasonable and constructive alternative is intellectually bankrupt. NEASA’s biggest failing is that it knows roughly what it is against, but has no credible positive programme to define and realize concrete policy objectives.

If only our problems were limited to hours of work and wages, how simple the road ahead would be in resolving these. At an aggregated level, compensation of employees makes up 20% of the total input costs to the metals and engineering sector. Should our focus and collaborative creative thinking not rather be on the 80% of the equation. The trouble is that even on these issues, NEASA has no real idea what to do to remedy them. It attacks all and sundry, but has no plan to get these issues addressed.

The future for this industry will be created by those who have the courage to take action.

NEASA quite simply doesn’t have what it takes to confront the challenges facing industry. NEASA is characterized by crass opportunism, hypocrisy and an authoritarian populism offering nothing to its followers.

NEASA may well have made gains in membership in recent years. This is good for our industry. Of course, the emergence of a credible alternative model addressing the plight of SMME’s would be even better. But since 2010, NEASA has centered its strategies on opposition to SEIFSA. But now that the Main Agreement has been gazetted and extended, NEASA suddenly look very shaky. The focus on SEIFSA leaves NEASA struggling for relevance in a post gazettal era. NEASA’s most recent Newsletter has the ring of desperation.

NEASA will have to develop a credible vision of the future that talks to the real challenges facing its membership on its own or in alliance with employer bodies across the spectrum and here’s the rub - in partnership with all stakeholders that NEASA over the years has been quick to point the finger of blame.

Deals or Agreements are not perfect, they are the product of negotiations and compromise. Reaching agreement with the other side whether in the commercial or industrial relations sphere is tough, walking away is easy. Continuing the engagement process when all else seems lost requires commitment, dedication and innovative and creative thinking.

SEIFSA representing 18 Employer Associations, with an 80-year track record of delivering industry solutions, employing close to 150 000 employees, is ready to work in partnership with all industry stakeholders, who understand, that deals are struck when adversaries arrive at the stark reality that time would be better spent on focusing on what they have in common instead of the issues that divide them.

Lucio Trentini

Chief Executive Officer

SAFTU’S Intended protest action 20 March 2023

Introduction

Management may be aware, from recent media reports, that the South African Federation of Trade Unions (SAFTU), of which NUMSA is a member, intends joining the Economic Freedom Fighters’ (EFF) call for a national shutdown on 20 March 2023.

Protest Action and the Labour Relations Act

The Labour Relations Act (LRA) permits registered trade unions or federations such as SAFTU, to undertake protected protest action to promote the social and economic interests of workers provided that they observe the procedural requirements contained in Section 77 (1) (b) of the LRA 66 of 1995, as amended.

This application was duly considered by NEDLAC and the NEDLAC Section 77 Standing Committee has determined the notice to be compliant with the administrative requirements of the LRA. SAFTU can therefore go on protest action based on their 1(b)-notice submitted in 2020, and their latest 1(d) notice. Procedurally, they have met the requirements.

Consequently, any employees participating in any action on 20th March will be protected by the normal rules regarding protected strike-action, namely: no-work-no-pay and no disciplinary action.

Management Guidelines on Possible Absenteeism on Monday, 20 March 2023

SEIFSA recommends that management adopt the following course of action in dealing with any stay-away from work on the 20th March:

- Inform all workers that any absences related to the protest action will be treated on the following basis:

- no work, no pay; no disciplinary action;

- a shift for leave-pay and leave-enhancement pay qualification purposes will be lost in respect of the day’s absence;

- any overtime worked during the course of the week will be paid at ordinary rates to make up for the lost ordinary working hours from Monday, 20th March February 2023; and

- Management is at liberty to explore the possibility of arranging mutually acceptable alternative work-in-time arrangements in view of the Monday being sandwiched between a week-end and a public holiday on the 21 March 2023.

The Staff of the SEIFSA Industrial Relations Division are available on (011) 298-9400 to provide any further advice and/ or assistance to management on the contents of this management brief.

BUSA on President Cyril Ramaphosa cabinet reshuffle

We note the announcement by President Ramaphosa of his reshuffled cabinet. The appointment of Dr Kgosientsho Ramokgopa as Minister of Electricity is a critical one and we will engage him urgently to see what his thinking is on dealing with the short-term loadshedding crisis and the medium-term energy crisis. We were of the view a new Minister of Electricity should not be appointed, but now that the President has appointed him, we will continue our support to help implement the President’s Energy Plan as a matter of urgency. He will have a significant challenge in coordinating roles between his department and that of the Minister of Resources and Energy and how he utilises the powers accorded to him under the State of Disaster.

Numerous new ministers are new people and we will wait to see what announcements they make about their plans and strategies and we will expect significant improvement in policy formulation and, particularly in implementation. We also expect to see a Cabinet that is aligned behind the President’s vision and one that speaks with a single voice.

The Cabinet will have to demonstrate, with urgency, that ministers will be moving with speed to address the numerous crises we are experiencing in our country. The ministers do not have the luxury of taking their time in getting into their roles, but must move with urgency and implement, implement, implement!

Business has consistently indicated its readiness to work with government to shift the needle significantly in attracting investment and putting our country onto a sustainable and inclusive growth path. We remain committed to pursue this and urge relevant ministers to collaborate with us in a real partnership.

We will look out with great interest for urgent indications from the Cabinet about its priorities in the next few weeks. We will, on the basis of such indications, engage and see if there are possibilities of working together. But we will also continue to hold Cabinet, and the President, to account to show decisive leadership and act with urgency to rebuild trust of government amongst South Africans and to instil confidence amongst investors.

ENDS

Cas Coovadia

Business Unity SA CEO