Metals and Engineering sector production continues to fall more than employment

JOHANNESBURG, 19 OCTOBER 2016 - Figures released by Statistics South Africa (StatsSA) today show production in the sector declined by 3,9% up to August this year, while employment numbers dropped by 3,1% over the same period. Over a 12-month period, production contracted by 4,9%, while employment has fallen by 2,2%.

Commenting on the data, SEIFSA Chief Economist Henk Langenhoven said that the latest production (August 2016) and employment data (second quarter 2016) show no relief in the economic contraction experienced by the metals and engineering sector.

“The great concern is that production is still falling faster than the employment shed over the first half of 2016. These numbers are in contrast to overall manufacturing, which recorded some improvement in production over the year to August 2016,” he said.

Mr Langenhoven said that it is obvious that the production performance of sub-industries in the metals and engineering sector paints a dire picture. Sub-industry figures show that:

- On a 12-month basis, only electrical machinery and equipment manufacturing registered growth of 3%, which is lower than the +5,5% recorded by the end of July this year.

- Over the eight months of 2016, electrical machinery and equipment grew by +0,3% (against 3% previously) and other fabricated metal production grew by +1,2% (against 0,5% in the previous period).

- Basic ferrous production was slightly up by 0,4%. All the other groupings contracted, resulting in the 3,9% decline.

- Of growing concern is that month-on-month performances have deteriorated for some time now. This year, August production was 2,5% lower than July production, which was 2,1% lower than June’s. Only other fabricated metals (+3,7%), general machinery (+1,6%) and household appliances production (+1,3%) increased.

Mr Langenhoven said that the employment survey was done in the middle of the second quarter of 2016. That quarter showed a slight 0,3% (equivalent to 1 044 people) improvement in employment numbers on the first quarter.

“This was in line with a slight improvement in activity during March and April this year, which unfortunately subsided again. Over the first six months period, employment declined by 3,1% on the last half of 2015, and by 2,2% over 12 months,” he added.

Regarding the drop in employment, Mr Langenhoven explained that over a year period (ending in June 2016) the sector recorded a loss of 8 521 jobs. Despite this disappointment, more jobs were created by the electrical machinery and equipment (+1 545), ship building (+297), railway rolling stock (+378), rubber (+501), plastics (+125) and metal castings (+12) sub-industries.

“As for future employment, perceptions are generally negative and in some industries extremely negative,” he said.

The employment indicator of the Barclays/Bureau for Economic Research (BER) purchasing managers’ index (shows a further decline of 3,8% in September this year, which was a continuation of the August 2016 pattern. The latter information covers the manufacturing sector as a whole).

The BER quarterly manufacturing survey differentiates amongst the different sub-industries in the metals sector.

Mr Langenhoven further said that analysis showed that all the sub-industries, bar electrical machinery and equipment (which was highly positive), showed negative sentiment regarding employment numbers towards the end of the year.

“Basic metals indicated some easing, but still had a negative outlook, while fabricated metals and machinery were highly negative about employment prospects. The plastics industry was slightly negative, with the outlook deteriorating towards the end of the year,” he explained.

Reiterating SEIFSA’s previous sentiments of concern, he added that confidence is deteriorating regarding the sector’s future performance, with implications of an extended period of decline.

“Indications are stronger now that these conditions will only improve towards the latter half of 2017. The latest production numbers point to such an outcome. All indications are that job losses will also not ease up for the foreseeable future,” Mr Langenhoven said.

Press Release - 2016/10/17: INDUSTRY VETERAN MICHAEL PIMSTEIN ELECTED SEIFSA PRESIDENT AHEAD OF 2017 WAGE NEGOTIATIONS

A Joint Chief Executive Officer of Capital Appreciation Limited and former CEO of Macsteel Service Centres SA, Mr Pimstein assumes the presidency of the Federation and the Chairmanship of its Board in a crucial year that will see wage negotiations taking place in the metals and engineering sector.

Mr Pimstein, who has previously served as SEIFSA President in 2006/7, replaces Transman Founder and CEO Angela Dick, who made history last year when she was elected SEIFSA’s first woman President.

At the AGM on Friday, ArcelorMittal South Africa Chief Marketing Officer Alph Ngapo and Aveng Group Employee Relations Manager Oupa Jacob Komane were elected SEIFSA Vice-Presidents. Also elected onto the new Board were Atlantis Foundries CEO Pieter du Plessis, Murray and Roberts (Power and Energy) Human Resources Executive Anthony Albert Boy and Arabela Holdings (Pty) Ltd Executive Chairman Elias Monage.

ABB South Africa CEO and former SEIFSA Vice-President Leon Viljoen continues into his second year as a member of the Board.

Mr Pimstein has more than 30 years’ experience as a senior executive in the steel, engineering and manufacturing sectors. He has also served as a member of various government, labour and business committees addressing industrial policy, growth and development plans, infrastructure requirements and investment, as well as in labour mediation and wage negotiations.

In his first address as president of the Federation on Friday, Mr Pimstein acknowledged the challenges currently confronting the South African economy in general and the metals and engineering sector in particular, and stressed the need for all SEIFSA member Associations and other stakeholders to work together.

“These difficult conditions are likely to prevail for some time since there are no signs that the world market is rapidly moving out of its weakness. We need to prepare ourselves in South Africa to do the best we can in a metals and engineering market that is not likely to exceed 4.5 million tons,” he said.

The University of the Witwatersrand’s Professor Susan Booysen was the guest speaker at SEIFSA’s Annual Presidential Breakfast, where she delivered an insightful address on the state of South African politics.

SEIFSA Chief Executive Officer Kaizer Nyatsumba congratulated the new Board Members.

“Colleagues and I welcome the new SEIFSA Board and the President and look forward to working with them. In them, the Federation is gaining a team with extensive and vast experience. I am confident that as we steer the metals and engineering sector through the current crisis and move toward negotiations, this Board will provide the necessary guidance and use its considerable leadership experience to instill confidence,” Mr Nyatsumba said.

State of the Metals and Engineering Sector 2017 to 2018

State of the Metals and Engineering Sector 2017 to 2018

This article is an extrapolated summary of the State of the Metals and Engineering Sector 2017 to 2018 Report. The current report is the fourth such report in as many years. The full report is available from SEIFSA.

GLOBAL ECONOMIC ENVIRONMENT

There is a general sense of optimism in the global economy as we enter 2017.

The high degree of uncertainty surrounding the economic policies of the new administration in the United States of America (USA) is expected to persist for some time, creating a challenging and volatile environment for emerging markets. The prospect of rising protectionism and its implications for world trade are also a concern. The impact of Brexit, how the separation will be managed, and if any more countries will leave the Union also pose a potential risk to global economic stability.

Prospects for a resumption of interest rate hikes in the USA remain and will be a key determinant to the pattern of global capital flows and to the rand. Hopefully this should be mitigated by the very accommodative monetary policy stances in the European Union and Japan.

Activity in advanced economies is expected to expand to 1.8% in 2017, up from 1.6% in 2016.

Emerging market developing economies expanded by an estimated 3.4% in 2016, according to the World Bank. Interestingly, commodity-exporting economies expanded at a markedly lower pace than commodity importers. This suggests resilient domestic demand, low commodity prices and generally accommodative macroeconomic policies in commodity-importing economies. It also suggests that the increase in the commodity prices has not fully translated to the benefit of the commodity exporters, raising questions into the cyclicality or structural probabilities of the commodity price increases. Growth in the emerging economies is expected to expand to 4.2% in 2017.

Table 1: Growth Rates (Global, Advanced and Emerging Economies)

Source: World Bank, Jan 2017

Commodity prices were significantly low at the start of 2016, but the majority of them recovered. This points to possible further momentum in 2017. This has improved growth prospects for commodity-producing emerging markets in particular, along with more favourable capital inflows. However, it is unclear how long these positive developments will continue. Several emerging markets and developing economies face the task of optimising on the recent commodity price increases, even if the surge is short lived.

Graph 1: Global Commodity Price Index

Source: SARB, Dec 2016

SOUTH AFRICAN ECONOMY

2016 was a very difficult year for the South African economy and, by extension, the metals and engineering sector. The economy grew by 0.4% in 2016 and potential output was downgraded to 1.3%. A negative output gap was recorded in 2016. Gross fixed capital formation remained negative, with general government contributing to this contraction as explained by fiscal consolidation.

Economic growth in South Africa is forecast at 1.2% in 2017 and 1.8% in 2018, against the backdrop of improved commodity prices and improving global activity. Sentiment towards emerging markets looks promising, given advanced economy uncertainty. Hopefully this should translate into some continued rand strength.

THE METALS AND ENGINEERING SECTOR

The metals and engineering sector is currently going through a deep structural adjustment, one which begun in 2007/08. This structural adjustment extended through to 2016, which was a particularly difficult year for both the sector and the South African economy in general.

2016 was particularly concerning given the renewed downward trajectory in the production, employment, investment and profit trends. In 2016 capacity utilisation for the overall sector increased marginally when compared to 2015 but, measured on its long- run trend, the index has been on a downward trajectory since 2014.

In 2016, production in the metals and engineering sector contracted by 2%, employment decreased by 1.7% and profit margins deteriorated substantially.

Employment in the sector is currently above its production level by about 3000 jobs, and given the historical characteristics of the labour market in the sector for clearing excess capacity, we draw attention to the prospect of further job losses in the sector into 2017.

There is clear statistical proof that the renewed downward pressure in the production index can be attributed to the production disruptions of 2014 (the five-month platinum mines strike and the month-long metals and engineering strike). The sector has clearly not recovered from these disruptions. More importantly, the disruptions appear to have adversely affected the long-run trends. This is particularly important because the sector will be negotiating a new wage deal in 2017. We highlight this as a definite risk because in the event of an unfortunate outcome (production disruption), a new, deeper downward spiral could be initiated, in the process spelling disaster!

THE LABOUR MARKET IN THE METALS AND ENGINEERING SECTOR

Labour market dynamics are complex, at best. However, labour is one of the costs over which companies have a relative degree of control. It would follow that in an environment where the sector is contracting, cost rationalisation and optimisation would most likely result in attempts to manage this line in the income statement. The strong correlation between production and employment affirms this synopsis.

There is a negative unit labour cost to labour productivity differential in the metals and engineering sector, an unfortunate trend which has held since 2009.

Investment into the sector has also been relatively low for reasons that include a flat economy, flat markets and idle capacity, to name a few. However, the capital labour ratio indicates that there has not yet been a significant drive to mechanise in the sector.

METALS AND ENGINEERING INTERNATIONAL TRADE

The international trade performance of the metals and engineering sector improved markedly when 2016 is compared to 2015, even though a trade deficit was recorded in 2016. Improvement was also recorded in the terms of trade in 2016.

The trade deficit receded in 2016, with the sector exporting R216 billion worth of output and importing R339 billion worth of product, resulting in a trade deficit of R122 billion. The sector’s terms of trade improved by 4.6% in 2016.

Regional trade baskets have remained unchanged, with Africa still counting as the highest export region for the sector. A decline of 9% in Africa’s share to the total export basket was recorded in 2016, which is indicative of the reliance of African economies on commodities and commodity prices, and how it affects their demand for imports (South African exports). In the composition of Africa as an export market, the South African Development Community (SADC) continues to be the largest export destination at 85%.

INPUT COST AND SELLING PRICE INFLATION

The input cost inflation prospects of the metals and engineering sector are to a great degree dependent on exchange rate movement. This is evident in the easing in input cost inflation as the exchange rate strengthened in the last quarter of 2016. This created a positive inflation differential between selling price and input cost inflation for the first time since the beginning of 2015.

2017 FORECAST

Our 2017 prognosis is for the metals and engineering sector to expand by 1.4% on an annualised quarterly average.

This is comparable to the calculation of GDP growth. However, 2016 was a very bad year therefore contributing statistical base effects in computing the result above. When we control for base effects, our model computes the metals and engineering sector expanding by 0.4% in 2017.

This improvement is a function of improving global and domestic growth. Commodity prices are an important link between developed and developing markets and are a channel of wealth distribution. The current commodity price surge contributes favourably to our forecast; however, there is a lot of uncertainty as to whether it is simply a cyclical bounce or a structural one. As at the beginning of 2017, all indications point to a cyclical bounce. This places greater responsibility on policy makers and companies to make the most of the commodity price surge, in what seems to be a fairly short time horizon.

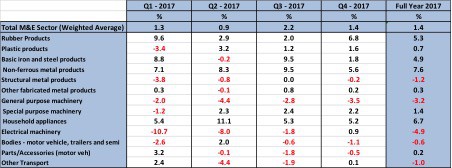

Table 2: M&E and Sub-Industry Forecasts

Source: SEIFSA Calculations

In our prognosis we stress the fact that our forecast is underpinned by an assumption of no production disruptions linked to the 2017 wage negotiations. In the event of strike action ensuing, we would have to revise our forecast model.

Industry Veteran Michael Pimstein elected SEIFSA President ahead of 2017 Wage Negotiations

Industry Veteran Michael Pimstein elected SEIFSA President ahead of 2017 Wage Negotiations

JOHANNEBURG, 17 October 2016 – Industry veteran Michael Pimstein was elected President of the Steel and Engineering Industries Federation of Southern Africa (SEIFSA) at the organisation’s Annual General Meeting (AGM) on Friday.

A Joint Chief Executive Officer of Capital Appreciation Limited and former CEO of Macsteel Service Centres SA, Mr Pimstein assumes the presidency of the Federation and the Chairmanship of its Board in a crucial year that will see wage negotiations taking place in the metals and engineering sector.

Mr Pimstein, who has previously served as SEIFSA President in 2006/7, replaces Transman Founder and CEO Angela Dick, who made history last year when she was elected SEIFSA’s first woman President.

At the AGM on Friday, ArcelorMittal South Africa Chief Marketing Officer Alph Ngapo and Aveng Group Employee Relations Manager Oupa Jacob Komane were elected SEIFSA Vice-Presidents. Also elected onto the new Board were Atlantis Foundries CEO Pieter du Plessis, Murray and Roberts (Power and Energy) Human Resources Executive Anthony Albert Boy and Arabela Holdings (Pty) Ltd Executive Chairman Elias Monage.

ABB South Africa CEO and former SEIFSA Vice-President Leon Viljoen continues into his second year as a member of the Board.

Mr Pimstein has more than 30 years’ experience as a senior executive in the steel, engineering and manufacturing sectors. He has also served as a member of various government, labour and business committees addressing industrial policy, growth and development plans, infrastructure requirements and investment, as well as in labour mediation and wage negotiations.

In his first address as president of the Federation on Friday, Mr Pimstein acknowledged the challenges currently confronting the South African economy in general and the metals and engineering sector in particular, and stressed the need for all SEIFSA member Associations and other stakeholders to work together.

“These difficult conditions are likely to prevail for some time since there are no signs that the world market is rapidly moving out of its weakness. We need to prepare ourselves in South Africa to do the best we can in a metals and engineering market that is not likely to exceed 4.5 million tons,” he said.

The University of the Witwatersrand’s Professor Susan Booysen was the guest speaker at SEIFSA’s Annual Presidential Breakfast, where she delivered an insightful address on the state of South African politics.

SEIFSA Chief Executive Officer Kaizer Nyatsumba congratulated the new Board Members.

“Colleagues and I welcome the new SEIFSA Board and the President and look forward to working with them. In them, the Federation is gaining a team with extensive and vast experience. I am confident that as we steer the metals and engineering sector through the current crisis and move toward negotiations, this Board will provide the necessary guidance and use its considerable leadership experience to instill confidence,” Mr Nyatsumba said.

Safety, Health, Environment & Quality FAQ

[faq state="closed" question="Why do employers have to comply with the OHS Act?"]Companies have a duty to comply with all company related legislation. This legislation includes various Acts of Parliament, including, but not limited to:

- Basic Conditions of Employment

- Labour Relations

- Occupational Health and Safety

- Compensation for Occupational Injuries and Diseases

- National Environmental

- Atmospheric Pollution Prevention

- National Building Standards Act

As with any legislation that is enforceable, the OHS Act carries heavy penalties for non-compliance. In general, a fine of R 50 000.00 or one year imprisonment, or both a fine and imprisonment can be given and where there is, or could have been, a charge of culpable homicide, then a fine of R 100 000.00 or two years imprisonment, or both can be given.[/faq]

[faq state="closed" question="What are the main duties of the employer in terms of the OHS Act?"]OHS Act Sect 8. General duties of employers to their employees:

(1) Every employer shall provide and maintain, as far as is reasonably practicable, a working environment that is safe and without risk to the health of his employees

(2) Without derogating from the generality of an employer's duty under subsection (1), the matters to which those duties refers include in particular:

(a) the provisions and maintenance of systems of work, plant and machinery that as far as is reasonably practicable, safe and without risks to health

(b) taking such steps as may be reasonably practicable to eliminate or mitigate any hazard or potential hazard to the safety or health of employees, before resorting to personal protective equipment

(c) making arrangements for ensuring, as far as is reasonably practicable, the safety and absence of risks to health in connection with the production, processing, use, handling, storage or transport of articles or substances

(d) establishing, as far as is reasonably practicable, what hazards to the health or safety of persons are attached to any work which is performed, any article or substance which is produced, processed, used, handled, stored or transported and any plant or machinery which is used in his business, and he shall, as far as is reasonably practicable, further establish what precautionary measures should be taken with respect to such work, article, substance plant or machinery in order to protect the health and safety of persons and he shall provide the necessary means to apply such precautionary measures

(e) providing such information, instructions, training and supervision as may be necessary to ensure as far as is reasonably practicable, the health and safety at work of his employees

(f) as far as is reasonably practicable, not permitting any employee to do any work or to produce, process, use, handle, store or transport any article or substance or to operate any plant or machinery, unless the precautionary measures contemplated in paragraphs (b) and (d) or any other precautionary measures which may be prescribed, have been taken

(g) taking all necessary measures to ensure that the requirements of this Act are complied with by every person in his employment or on premises under his control where plant or machinery is used

(h) enforcing such measures as may be necessary in the interest of health and safety

(i) ensuring that work is performed and that plant or machinery is used under the general supervision of a person trained to understand the hazards associated with it and who have the authority to ensure that precautionary measures taken by the employer are implemented and

(j) causing all employees to be informed regarding the scope of their authority as contemplated in section 37 (1)(b).[/faq]

[faq state="closed" question="What is the most critical part of the employer’s duties?"]To identify all hazards in the workplace, assess the risks associated with the hazards, determine what precautionary measures are needed to protect the health and safety of employees and others, implement those precautionary measures and train employees to work safely, following the health and safety systems, procedures and rules.[/faq]

[faq state="closed" question="Do employees also have duties in terms of the OHS Act?"]OHS Act Sect 14. General duties of employees at work

Every employee at work should:

- take reasonable care for the health and safety of himself and of other persons who may be affected by his acts or omissions

- as regards any duty or requirement imposed on his employer or any other person by this Act, co-operate with such employer or person to enable that duty or requirement to be performed or complied with

- carry out any lawful order given to him and obey the health and safety rules and procedures laid down by his employer or by anyone authorised thereto by his employer, in the interest of health or safety

- if any situation which is unsafe or unhealthy comes to his attention, as soon as practicable report such situation to his employer or to the health and safety representative for his workplace or section thereof, as

- the case may be, who shall report it to the employer and

- if he is involved in any incident which may affect his health or which has caused an injury to himself, report such incident to his employer or to anyone authorised thereto by the employer, or to his health and

- safety representative, as soon as practicable but not later than the end of the particular shift during which the incident occurred, unless the circumstances were such that the reporting of the incident was not

- possible, in which case he shall report the incident as soon as practicable thereafter.[/faq]

[faq state="closed" question="Our company uses the services of an independent contractor to perform certain activities at the workplace. The contractor occasionally uses casual labour to assist him with the work. Must the contractor be registered with the Compensation Fund?"]Yes. An employer is defined by the Compensation for Occupational Injuries and Diseases Act as “any person, including the State, who employs an employee”. A closer look at the definition of an employee in terms of the Act includes casual employees (i.e. a person employed for less than 24 hours in a month). The contractor must also be registered with the Department of Labour in terms of the UIF, with SARS and where necessary, the Metal and Engineering Industries Bargaining Council.[/faq]

[faq state="closed" question="Which occupational injuries must be reported to the Compensation Commissioner?"]OHS Act Sect 24. Report to inspector regarding certain incidents

(1) Each incident occurring at work or arising out of or in connection with the activities of persons at work or in connection with the use of plant or machinery in which, or in consequence of which :

(a) any person dies, becomes unconscious, suffers the loss of a limb or part of a limb or is otherwise injured or becomes ill to such a degree that he is likely either to die or to suffer a permanent physical defect or likely to be unable for a period of at least 14 days either to work or to continue with the activity for which he was employed or is usually employed

(b) a major incident occurred or

(c) the health or safety of any person was endangered and where

(i) a dangerous substance was spilled

(ii) the uncontrolled release of any substance under pressure took place

(iii) machinery or any part thereof fractured or failed resulting in flying, falling or uncontrolled moving objects or

(iv) machinery ran out of control, shall, within the prescribed period and in the prescribed manner, be reported to an inspector by the employer or the user of the plant or machinery concerned, as the case may be

(2) In the event of an incident in which a person died, or was injured to such an extent that he is likely to die, or suffered the loss of a limb or part of a limb, no person shall without the consent of an inspector disturb the site at which the incident occurred or remove any article or substance involved in the incident therefrom: Provided that such action may be taken as is necessary to prevent a further incident, to remove the injured or dead, or to rescue persons from danger

(3) The provisions of subsections (1) and (2) shall not apply in respect of -

(a) a traffic accident on a public road

(b) an incident occurring in a private household, provided the householder forthwith reports the incident to the South African Police or

(c) any accident which is to be investigated under section 12 of the Aviation Act , 1962 (Act No. 74 of 1962)

(4) A member of the South African Police to whom an incident was reported in terms of subsection (3)(b), shall forthwith notify an inspector thereof.

OHS Act General Administrative Regulations Sect 8. Reporting of incidents and occupational diseases

(1) An employer or user, as the case may be, shall:

(a) within seven days of any incident referred to in section 24(1)(a) of the Act, give notice thereof to the provincial director in the form of WCL1 or WCL 2; and

(b) where a person, in consequence of such an incident, dies, becomes unconscious, suffers the loss of a limb or part of a limb, or is otherwise injured or becomes ill to such a degree that he or she is likely either to die or to suffer a permanent physical defect, such incident, including any other incident contemplated in section 24(1)(b) and (c) of the Act, shall forthwith also be reported to the provincial director by telephone, facsimile or similar means of communication

(2) If an injured person dies after notice of the incident in which he or she was injured was given in terms of subregulation (1), the employer or user, as the case may be, shall forthwith notify the provincial director of his or her death

(3) Whenever an incident arising out of or in connection with the activities of persons at work occur to persons other than employees, the user, employer or self-employed person, as the case may be, shall forthwith notify the provincial director by facsimile or similar means of communication as to the :

(a) name of the injured person

(b) address of the injured person

(c) name of the user, employer or self-employed person

(d) address of the user, employer or self-employed person

(e) telephone number of the user, employer or self-employed person

(f) name of contact person

(g) details of incident:

(i) What happened

(ii) where it happened (place)

(iii) when it happened (date and time)

(iv) how it happened

(v) why it happened and

(h) names of witnesses

(4) Any registered medical practitioner shall, within 14 days of the examination or treatment of a person for a disease contemplated in section 25 of the Act, give notice thereof to the chief inspector and the employer in the form of WCL 22

(5) Any other person not contemplated in this regulation may in writing give notice of any disease contemplated in section 25 of the Act, to the employer and chief inspector

A delay to report an accident or an alleged accident is a criminal offence and the Commissioner may impose a penalty on the employer which could be equivalent to the full amount of the claim.[/faq]

[faq state="closed" question="What is the procedure when reporting an occupational injury?"]

The employer is liable to pay the employee 75% of his/her earnings for the first three months from the date of the injury. The employer will then be reimbursed by the Compensation Fund. Many employers still pay their employees 100% of their earnings for this period. However, keep in mind that the Fund will only reimburse 75% of monies paid to the employee.

A certified copy of the employee’s identity document must accompany the registration of a claim with the Fund. If a copy of the ID is not submitted, the claim will not be registered and will be returned to the employer. All other documentation submitted to the Fund must also reflect the employee’s ID number.

Employers will need to report the incident on a W.CL.2 form. “Part A” of the form (pages 1 and 2) must be completed as comprehensively as possible, including the date of the incident and a signature and then forwarded to the Compensation Commissioner without delay. “Part B” must be detached from the form and given to the injured employee to take to the doctor or hospital concerned.

The Fund will consider the claim when it receives the W.CL.2 form and a First Medical Report (W.CL.4). If liability is accepted, a postcard (W.CL.56) will be forwarded to the employer by mail reflecting the claim number. The employer will not be able to follow up on the progress of the claim until a claim number has been allocated.

[/faq]

[faq state="closed" question="I have heard about reporting an injury telephonically. How do I do this?"]

To expedite the finalisation of a claim, employers have the option to report injuries to the Compensation Fund telephonically. However, an employer must register to enable the company to report incidents telephonically. Documentation known as the TR2 Form and TR2 Card must be completed.

The advantage of reporting telephonically is that a claim number is allocated when you report the incident, long before any documentation has been mailed.[/faq]

[faq state="closed" question="Is the employer responsible for transporting an injured employee to the doctor and/or hospital for further treatment, check-ups or physiotherapy?"]Yes. The reasonable expenses incurred for conveying an employee injured in an accident to a hospital or to his residence will be refunded by the Compensation Fund. The employer can agree to pay the travelling costs to the employee and then claim it back from the Fund[/faq]

[faq state="closed" question="Does the company need to investigate these incidents?"]

(1) An employer or user shall keep at a workplace or section of a workplace, as the case may be, a record in the form of Annexure 1 for a period of at least three years, which record shall be open for inspection by an inspector, of all incidents which he or she is required to report in terms of section 24 of the Act and also of any other incident which resulted in the person concerned having had to receive medical treatment other than first aid

(2) An employer or user shall cause every incident which must be recorded in terms of subregulation

(1), to be investigated by the employer, a person appointed by him or her, by a health and safety representative or a member of a health and safety committee within 7 days from the date of the incident and finalised as soon as is reasonably practicable, or within the contracted period in the case of contracted workers

(3) The employer or user shall cause the findings of the investigation contemplated in subregulation

(1) to be entered in Annexure 1 immediately after completion of such investigation

(4) An employer shall cause every record contemplated in subregulation

(1) to be examined by the health and safety committee for that workplace or section of the workplace at its next meeting and shall ensure that necessary actions, as may be reasonable practicable, are implemented and followed up to prevent the recurrence of such incident.

[/faq]

Human Capital & Skills Development FAQ

Frequently Asked Question(s) FAQ, s

- What is the purpose of the Skills Development Act?

The short supply of skilled staff is a serious obstacle to the competitiveness of industry in South Africa. The Skills Development Act of 1998 aims to:

• Develop skills for the South African work force;

- Increase investment in education and training, and improve return on investments in those areas

- Encourage employers to promote skills development by using the workplaces an active learning environment;

- Encourage workers to participate in learnership and other training programmes;

- Improve employment prospects by redressing previous disadvantages

- through training and education;

- Ensure the quality of education and training in and for the workplace, and

- Assist with the placement of first time work-seekers

The Skills Development Act aims to develop the skills of the South African workforce and to improve the quality of life of workers and their prospects of work.To improve productivity in the workplace and the competitiveness of employers and to promote self-employment.

- What is the aim of the skills development levy?

The levy grant scheme, legislated through the Skills Development Levies Act, 1999, serves to fund the skills development initiative in the country. The intention is to encourage a planned and structured approach to learning, and to increase employment prospects for work seekers. Participating fully in the scheme will allow you benefit from incentives and to reap the benefits of a better skilled and more productive workforce.

- What is the purpose of a Workplace Skills Plan (WSP)?

The Workplace Skills Plan serves to structure the type and amount of training for the year ahead, and is based on the skills needs of the organisation. A WSP should consider current and future needs, taking into account gaps identified through a skills audit, the performance management system, succession planning initiatives, and any new process or technology changes planned for the year.

Management discusses the company’s goals with employees who in turn commit to the process of achieving these goals. Management gets the opportunity to discover talent as well as skills that they did know that they had.

- What is an Annual Training Report (ATR)?

This report consists of all attendance registers, proof of expenditure, training provider used in this report the SETA can establish whether training was done or is in the process of being done.

- Does one get a percentage of monies spent on training?

- Mandatory grants are a refund against all monies contributed towards the skills development levy and not on monies spent on training.

- What is a learnership?

A learnership is a work-based learning programme that leads to a nationally recognised qualification. Thus, learners is in learnership programmes have to attend classes at a college or training centre to complete classroom-based learning, and they also have to complete on-the-job training in a workplace. This means that unemployed people can only participate in a Learnership programme, if there is an employer that is willing to provide the required work experience. A Learnership is aligned to the NQF and is usually between 12 and 18 Months in duration. Learners are paid a Stipend from the applicable SETA.

- Who must pay the levy?

The levy is calculated as 1% of your wage bill, payable monthly. All employers who are registered with the South African Revenue Service (SARS) for PAYE and have an annual payroll in excess of R500 000 must register with SARS to pay for the skills development levy.

- What are the requirements for claiming back Discretionary Grants?

Each funding window has a different set of rules, which will be communicated to companies. For further details, please contact the relevant SETA.

- How does an employer register for the levy?

Every employer who is liable to pay the levy must register with SARS by completing the registration form, Form SDL 101, which is available from all SARS offices. In order to register the employer must:

- Obtain a registration form (SDL 101) from any SARS office, if not received by mail;

- Choose from a list of registered Sector Education and Training Authorities (SETAs) as indicated in the SETA classification guide provided with the registration form, the one SETA most representative of your activities, and

- Choose a standard industry code (SIC) from the SETA classification guide which most accurately describes the nature and scope of your business

- To whom are levies payable?

Levies are payable to the South African Revenue Service, which acts as a collecting agency for the applicable SETA.

- By when is the levy payable?

The levy must be paid to SARS not later than SEVEN days after the end of the month in respect of which the levy is payable, under cover of a SDL 201 return form.

- Is there any interest and penalty incurred for late or non-payment?

SARS will impose both interest and penalties for late or non-payment of levies.

- How do I register as a Skills Development Facilitator?

You can use the online Skills Development Facilitator registration form via the relevant SETAs website or contact your regional co-ordinator. Your registration will be acknowledged as soon as it is processed.

- What is PIVOTAL Grant

PIVOTAL is an acronym which means professional , vocational technical and academic learning programme that result in a qualification or part qualification on the National Qualification Framework (NQF).

- What is SIPS?

SIPS is an acronym which means Strategic Infrastructure Projects

- What is meant by OFO?

OFO is an acronym which means Organising Framework for Occupations

- What is meant by NQF?

The NQF is organised as a series of levels of learning achievement, arranged in ascending order from one to ten. Each level on the NQF is described by a statement of learning achievement known as Level Descriptors (below).

There is one set of level descriptors for the NQF.

The NQF is a single integrated system which comprises of three co-ordinated qualifications Sub-Frameworks. These are:

- General and Further Education and Training Sub-Framework (GFETQSF)

- The Higher Education Qualifications Sub-Framework (HEQSF)

- The Occupational Qualifications Sub-Framework (OQSF)

The Sub-Frameworks have qualifications registered at the following NQF levels:

- GFETQSF - levels 1 to 4;

- HEQSF - levels 5 to 10;

- OQSF - levels 1 to 6.

- For NQF levels 7 and 8 the Quality Council for Trades and Occupations can motivate for a qualification only in collaboration with a recognised professional body and the Council on Higher Education, in a process co-ordinated by SAQA.

FAQ

[heading size="h5"]Human Capital & Skills Development FAQ[/heading]

We are a small company, our total leviable amount paid to all employees during a 12 month period does not exceed R500 000.00. In our 11 years of existence it never has and probably never will exceed. Do we still have to register and pay the Skills Development Levy (SDL)?

View Human Capital & Skills Development FAQs

[heading size="h5"]Safety, Health, Environment & Quality FAQ[/heading]

Why do employers have to comply with the OHS Act?

View Safety, Health, Environment & Quality FAQs

[heading size="h5"]Industrial Relations FAQ[/heading]

We have employees working from 06h00 on weekends. Their normal tea time is from 10h00 to 10h30 and lunch time is from 13h00 to 13h30. Some of the employees take additional breaks from 18h00 to 18h30 and then go home at 19h00. I know that according to the Basic Conditions of Employment Act they are entitled to a half-hour break for every five hours worked, but what does the Main Agreement say on this?

[heading size="h5"]Economic & Commercial FAQ[/heading]

What is the best indices to monitor price increase in the food /catering industry?

SEIFSA Economist on the Money Talk: 3% Decline in demand for Steel and Impact

SEIFSA Economist on the Money Talk: 3% Decline in demand for Steel and Impact

Tafadzwa Chibanguza, SEIFSA Senior Economist, featured on the Moneyweb's Money Talk on Radio 2000 with Tumisang Ndlovu where he illustrated the challenges of the 3% decline in the demand for steel products. Click here to listen.

{podcast id=1}

SEIFSA Senior Economist, Tafadzwa Chibanguza

Watch SEIFSA Senior Economist, Tafadzwa Chibanguza, discuss the warning announcement by S&P about a possible downgrade of the local economy to junk status and the impact around such.

SEIFSA CAUTIOUSLY WELCOMES CPI REPRIEVE WHICH RELIEVES CONSUMERS

The headline consumer price index annual inflation for August 2016 is 5.9%, marginally down by 0.1 of a percentage point from 6% in the same period last year. This decreased prices by 0.1% between July 2016 and August 2016, trimming only slight pressure off consumers. Core inflation – which excludes food, petrol and energy prices – recorded a 5.7% increase over a comparable period, maintaining the same reading as a month earlier.

Commenting on the latest figures, SEIFSA Economist Tafadzwa Chibanguza welcomed the existence of an underlying trend of inflationary reprieve, saying that consumers will welcome the much-needed relief, albeit minimal.

“Consumers have been under a lot of financial pressure in the last few months and the latest reading on consumer inflation from StatsSA will offer some much-needed reprieve,” Mr Chibanguza said.

However, Mr Chibanguza said that this emerging picture should be viewed with a degree of caution since both readings (headline and core) place at the upper edge of the South African Reserve Bank’s inflation target of 3% to 6%.

Mr Chibanguza said the main contributor to the annual inflationary decrease was the transport sub-component, which decreased two basis points as a result of an average 7.2% decrease between petrol and diesel prices. At the same time, the recreation and culture component increased one basis point in the comparable period, resulting in the net one basis point decrease in the August 2016 annual reading.

He said that the strength of the Rand against the US Dollar in August also contributed significantly to the inflation outcome.

Since the end of June, the Rand had been on a strong recovery path, with the strongest points being recorded in August. Over this period, the currency recovered by 12.7%, trading below $1/R14 for the first 24 days of August.

“This undoubtedly contributed to the August 2016 reprieve. Unfortunately, it would not take a lot of factors to go wrong to reverse the trend and place us outside of the upper end of the target range,” Mr Chibanguza said.

He said that continuation of the current scenario – with the Rand/Dollar exchange rate below $1/R14 and strengthening, Brent crude oil trading below $50/barrel, a weak economy and consumers still being under pressure – was likely to lead to the Monetary Police Committee (MPC) of the Reserve Bank leaving the interest rate unchanged at the conclusion of its meeting tomorrow.

“The inflation reading announced today would give the MPC one more reason to hold back from a rates increase for now, providing further relief to the consumer,” Mr Chibanguza concluded.

SEIFSA welcomes slight improvement in the CPI

SEIFSA WELCOMES SLIGHT IMPROVEMENT IN THE CPI

JOHANNEBURG, 15 February 2017

The Steel and Engineering Industries Federation of Southern Africa (SEIFSA) today welcomed the marginal reprieve in the Consumer Price Index (CPI) and expressed confidence that its forecast of a 1,4% growth in the sector for the year was on track.

Data released by Statistics South Africa (StatsSA) indicate that the January 2017 CPI fell by 0.2 percentage points (from 6,8% to 6.6%) in December 2016. This is the first decline in the past four months. This reading is on par with StatsSA forecast of 6.6%, revised up from 6.1% in their 2017 forecast.

SEIFSA Economist Roberta Noise said that although the 0.2 percent drop is a positive development, the 6.6% CPI is still the highest in the past seven years, with the last highest reading of 8.1% having been in January 2009 when compared on a year-on-year basis. At 6,4%, this is also the highest annual average for the year since 2009, during which CPI averaged 7.1%.

“These statistics simply reflect the severity of the impact on consumer prices caused by the El Nino drought on the back of volatility in petrol prices during 2016. Regrettably, the CPI has stubbornly remained outside the Reserve Bank’s target range of 3% - 6% throughout most of 2016,” said Ms Noise.

According to StatsSA, significant contributors to the latest CPI improvement include food and non-alcoholic beverage (0.3), transport (0.2) and miscellaneous goods (0.1) on a month-to-month comparison. The 50c/l petrol price increase in January 2017 is the main contributor to the increase of 1,5% in transport on a month-on-month basis as a direct result of the reduction in the supply of Brent Crude oil, which has been cut by 600 000 barrels per day following the December OPEC agreement.

On the other hand, core inflation for January 2017 was recorded at 5.7% when compared to January 2016, which excludes volatile variables such as food and fuel. Ms Noise said that this provides a more stable indication of consumer price movements.

Ms Noise said she was alarmed that inflation increased on a year-on-year basis by 0.6 percentage points when January 2017 (6.6%) is compared to January 2016 (6.2%).

Although this pattern is expected to continue in 2017, StatsSA forecasts indicate that CPI should ease in the last quarter of 2017 and fully return to the 3% - 6% target range in 2018.

“Such a scenario may indicate some light in the horizon for the metals and engineering sector, affirming SEIFSA’s forecast that the sector would grow by 1.4% in the 2017/2018 period,” said Ms Noise.